Chapter 5 Causalidad de Granger, Modelos Multivariados de Vectores Autoregresivos y de Cointegración, y Modelos ARDL

En este capítulo removeremos el supuesto de que el análisis es univariado, ya que introduciremos la posibilidad de que los procesos generadores de datos compartan información entre dos o más series. Como primera aproximación desarrollaremos el concepto de Causalidad de Granger. Mediante esta metodología discutiremos cuándo dos series se causan estadísticamente. Posteriormente, introduciremos una técnica más sofisticada conocida como la metodología de Vectores Autoregresivos (VAR), la cual es una generalización de los procesos Autoregresivos (AR) que analizamos al principio del curso. Finalmente, introduciremos la técnica de cointegración y de rezagos distribuidos (ARDL) para los casos en que las series que analicemos sean procesos no estacionarios.

A partir de este punto, asumiremos que las series empleadas son estacionarias en sus primeras diferencias y solo nos preocuparemos por su estacionariedad en los casos particulares de Cointegración y los modelos ARDL.

5.1 Causalidad de Granger

Hasta ahora hemos supuesto que una serie puede ser explicada únicamente con la información contenida en ella misma. No obstante, en adelante trataremos de analizar el caso en el que buscamos determinar relaciones entre variables y cómo el comportamiento de una serie influye en las demás. Algunas relaciones más importantes son las llamadas: causalidad. En este caso analizaremos el procedimiento de Granger (1969), conocido como causalidad de Granger. En adelante asumiremos que las series involucradas son débilmente estacionarias.

Sean \(X\) y \(Y\) dos series débilmente estacionarias. Definamos a \(I_t\) un conjunto de toda la información disponible hasta el momento \(t\). Asimismo, digamos que \(\overline{X}_t\) y \(\overline{Y}_t\) son los conjuntos de toda la información disponible (actual y pasada) de \(X\) y \(Y\), respectivamente. Es decir: \[\begin{eqnarray*} \overline{X}_t & := & \{ X_t, X_{t-1}, X_{t-2}, \ldots \} \\ \overline{Y}_t & := & \{ Y_t, Y_{t-1}, Y_{t-2}, \ldots \} \\ I_t & := & \overline{X}_t + \overline{Y}_t \end{eqnarray*}\]

Adicionalmente, definamos \(\sigma^2(*)\) como la varianza del término de error estimado de una regresión dada. Dicho lo anterior, digamos que:

La definición anterior aplica de igual forma si se reemplaza a \(X\) por \(Y\) y a \(Y\) por \(X\), respectivamente. De acuerdo a la definición anterior, existen 5 diferentes posibilidades de relaciones causales entre las dos series:

Por lo anterior, representaremos mediante un \(AR(p)\) con variables exógenas lo siguiente: \[\begin{equation} A(L) \begin{bmatrix} Y_t \\ X_t \end{bmatrix} = \begin{bmatrix} a_{11}(L) & a_{12}(L) \\ a_{21}(L) & a_{22}(L) \end{bmatrix} \begin{bmatrix} Y_t \\ X_t \end{bmatrix} = \begin{bmatrix} V_t \\ U_t \end{bmatrix} (\#eq:GrangerEq) \end{equation}\]

O en su versión \(MA(q)\) con variables exógenas: \[\begin{equation} \begin{bmatrix} Y_t \\ X_t \end{bmatrix} = B(L) \begin{bmatrix} V_t \\ U_t \end{bmatrix} = \begin{bmatrix} b_{11}(L) & b_{12}(L) \\ b_{21}(L) & b_{22}(L) \end{bmatrix} \begin{bmatrix} V_t \\ U_t \end{bmatrix} \end{equation}\]

Para determinar el test de causalidad utilizaremos una especificación similar a la de la ecuación (??). Para probar si \(X\) causa a \(Y\), consideraremos la siguiente regresión: \[\begin{equation} Y_t = \alpha_0 + \sum^{k_1}_{k = 1} a^k_{11} Y_{t-k} + \sum^{k_2}_{k = k_0} a^k_{12} X_{t-k} + U_{1,t} \end{equation}\]

Donde \(k_0 = 1\) y, en general, se asume que \(k_1 = k_2\). Asimismo, el valor de estas constantes se puede determinar con el criterio de Akaike (o cualquier otro criterio de información). No obstante, algunos autores sugieren que una buena práctica es considerar valores de \(k_1\) y \(k_2\) que recorran al 4, 8, 12 y 16.

Dicho lo anterior, el test de causalidad de Granger se establece con una prueba F, en la cual se prueba la siguiente hipótesis nula: \[\begin{equation} H_0: a^1_{12} = a^2_{12} = \ldots = a^{k2}_{12} = 0 \end{equation}\]

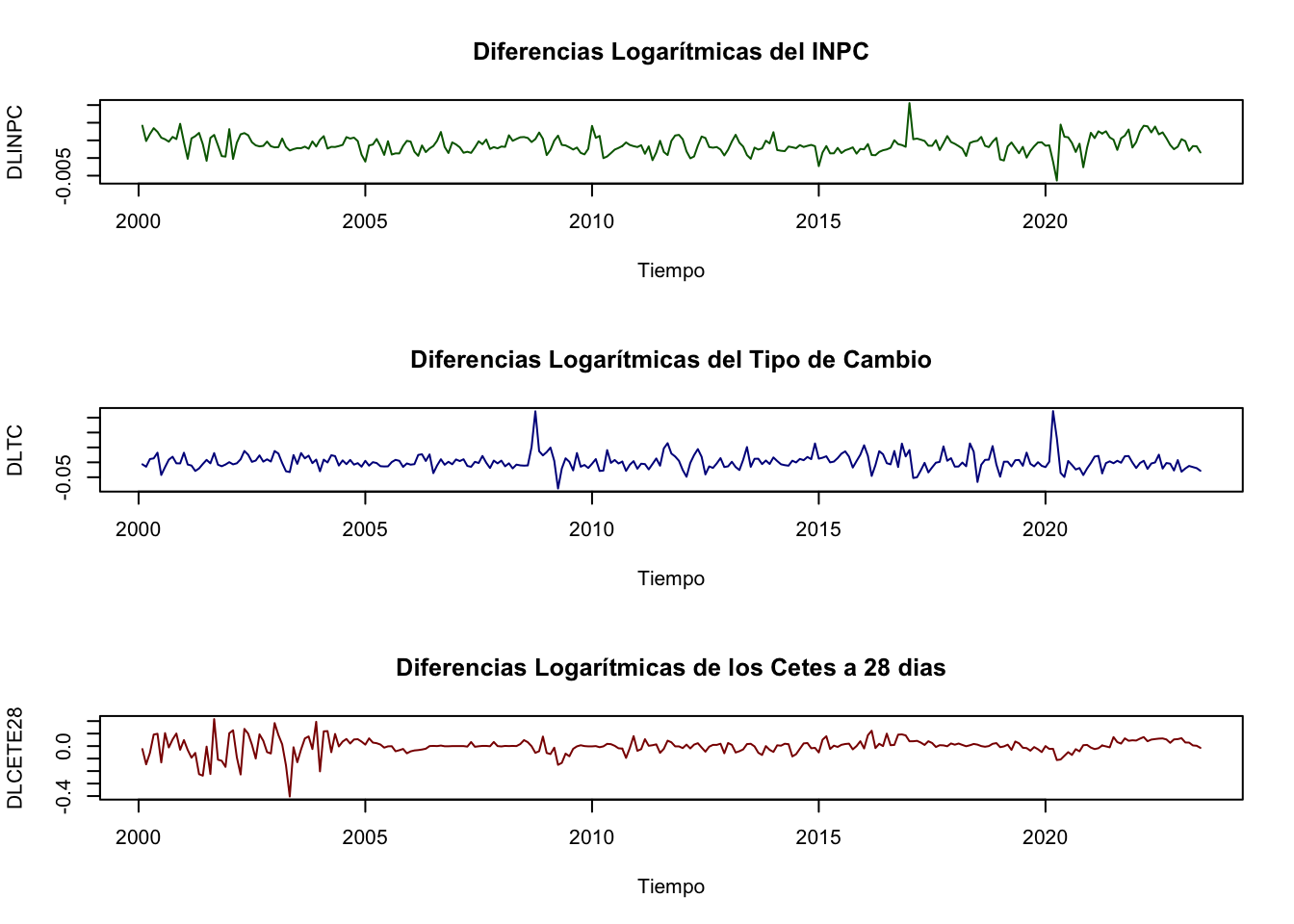

. Consideremos como variables analizadas al Índice Nacional de Precios al Consumidor (\(INPC_t\)), al Tipo de Cambio (\(TDC_t\)) y al rendimiento anual de los Cetes a 28 días (\(CETE28_t\)), todas desestacionalizadas para el periodo de enero de 2000 a julio de 2019. Dado que la metodología de Granger supone que las series son estacionarias, utilizaremos las diferencias logarítmicas de cada una de las tres series (es decir, utilizaremos una transformación del tipo \(ln(X_t) - ln(X_{t-1})\)). La Figura 5.1 muestra las series en su transformación de diferencias logarítmicas.

library(ggplot2)

library(dplyr)

library(stats)

library(MASS)

library(strucchange)

library(zoo)

library(sandwich)

library(urca)

library(lmtest)

library(vars)

#

load("BD/Datos_Ad.RData")

#

INPC <- ts(Datos_Ad$INPC_Ad,

start = c(2000, 1),

freq = 12)

DLINPC <- diff(log( ts(Datos_Ad$INPC_Ad, start = c(2000, 1), freq = 12) ))

TC <- ts(Datos_Ad$TC_Ad,

start = c(2000, 1),

freq = 12)

DLTC <- diff(log( ts(Datos_Ad$TC_Ad, start = c(2000, 1), freq = 12) ))

CETE28 <- ts(Datos_Ad$CETE28_Ad,

start = c(2000, 1),

freq = 12)

DLCETE28 <- diff(log( ts(Datos_Ad$CETE28_Ad, start = c(2000, 1), freq = 12) ))#

#png("Plots/DLGranger.png", width = 800, height = 1200)

par(mfrow=c(3, 1))

plot(DLINPC, xlab = "Tiempo",

main = "Diferencias Logarítmicas del INPC",

col = "darkgreen")

plot(DLTC, xlab = "Tiempo",

main = "Diferencias Logarítmicas del Tipo de Cambio",

col = "darkblue")

plot(DLCETE28, xlab = "Tiempo",

main = "Diferencias Logarítmicas de los Cetes a 28 dias",

col = "darkred")

Figure 5.1: Series en diferencias logarítmicas dadas por las siguientes expresiones: \(DLINPC_t = ln(DLINPC_t) - ln(DLINPC_{t-1})\), \(DLTC_t = ln(TC_t) - ln(TC_{t-1})\) y \(DLCETE28_t = ln(CETE28_t) - ln(CETE28_{t-1})\).

Por simplicidad, en el Cuadro 5.1 se muestra el resultado de aplicar el test de Granger a diferentes especificaciones, con rezagos 4, 8, 12 y 16, sólo para la serie de Tipo de Cambio en diferencias logarítmicas. En cada una de las pruebas se compara el modelo considerado como regresor a la variable que es candidata de causar, respecto del modelo sin considerar a dicha variable.

| Rezagos | Estadiística F | Probabilidad (\(>\)F) | Significancia |

|---|---|---|---|

| 4 | 3.2621 | 0.01265 | * |

| 8 | 1.9079 | 0.06030 | |

| 12 | 2.2577 | 0.01067 | * |

| 16 | 1.6735 | 0.05495 | * |

| Notas: | *** | signif. | al 0.1% |

| ** | signif. | al 1% | |

| * | signif. | al 5% |

De acuerdo con el Cuadro 5.1, podemos concluir que existe información estadísticamente significativa para concluir que la inflación causa a la tasa de depreciación cambiaria, ambas medidas como las diferencias logaritmicas. El resto de los resultados para las otras combinaciones de causalidad se encuentran en el R Markdown llamado Clase 13 ubicado en el repositorio de GitHub.

5.2 Definición y representación del Sistema o Modelo de Vectores Autorregresicos (VAR(p))

En esta sección ampliaremos la discusión planteada en el apartado anterior. En el sentido de que en la sección pasada nuestra discusión se limitó al análisis de causalidad entre dos variables a la vez, que si bien es posible extenderlo a más variables, es un procedimiento limitado a casos particulares por las siguientes razones.

El procedimiento de causalidad de Granger supone que es posible identificar un sistema de ecuaciones que debe conformarse una vez que se ha identificado el sentido de la causalidad. Así, el proceso anterior necesita del conocimiento previo de las relaciones que existen entre las variables.

Adicionalmente, no resuelve el problema más general que está relacionado con cómo identificar la causalidad cuando se tienen múltiples variables con múltiples sentidos de causalidad. En esta sección analizaremos una mejor aproximación al problema de cómo identificar la causalidad múltiple. Por lo tanto, como mecanismo para solucionar el problema planteado, analizaremos el caso de un Sistema o Modelo de Vectores Autoregresivos conocido como VAR.

El primer supuesto del que partiremos es que existe algún grado de endogeneidad entre las variables consideradas en el análisis. Adicionalmente, el segundo supuesto que estableceremos es que requerimos que las variables que tengamos consideradas sean estacionarias.

Por lo anterior, diremos que un modelo de Vectores Autoregresivos (VAR) es un procedimiento que sigue fundado en el supuesto de que las variables consideradas son estacionarias. Así, hasta este momento del curso hemos pasado de modelos univariados a modelos multivariados, pero no hemos podido dejar de asumir que las series son estacionarias.

En lo subsecuente asumiremos que las series empleadas son estacionarias y sólo lo demostraremos cuando, en su caso, sea necesario. Esto no significa que el lector deba asumir estacionariedad. Por el contrario, siempre debe probar que las series son estacionarias antes de iniciar la implementación de cualquier técnica de series de tiempo.

Ahora bien, iniciaremos con el establecimiento de la representación del proceso. Digamos que tenemos un proceso estocástico \(\mathbf{X}_t\) estacionario vectorial de dimensión \(k\): \[\begin{equation*} \mathbf{X}_t = \begin{bmatrix} X_{1t} \\ X_{2t} \\ \vdots \\ X_{kt} \end{bmatrix} \end{equation*}\]

Para cualquier \(i = 1, 2, \ldots, p\): \[\begin{equation*} \mathbf{X}_{t-i} = \begin{bmatrix} X_{1t-i} \\ X_{2t-i} \\ \vdots \\ X_{kt-i} \end{bmatrix} \end{equation*}\]

Donde cada \(X_{kt}\) en \(\mathbf{X}_t\) es una serie de tiempo por sí misma. De esta forma, la expresión reducida del modelo o el proceso \(VAR(p)\) estará dado por: \[\begin{equation} \mathbf{X}_t = \boldsymbol{\delta} + A_1 \mathbf{X}_{t-1} + A_2 \mathbf{X}_{t-2} + \ldots + A_p \mathbf{X}_{t-p} + \mathbf{U}_{t} (\#eq:VARp) \end{equation}\]

Donde cada uno de las \(A_i\), \(i = 1, 2, \ldots, p\), son matrices cuadradas de dimensión \(k\) y \(\mathbf{U}_t\) representa un vector de dimensión \(k \times 1\) con los residuales en el momento del tiempo \(t\) que son, por individual, un proceso puramente aleatorio. También se incorpora un vector de términos constantes denominado como \(\mathbf{\delta}\), el cual es de dimensión \(k \times 1\).

Así, la ecuación (??) supone la siguiente estructura del vector \(\boldsymbol{\delta}\): \[\begin{equation*} \boldsymbol{\delta} = \begin{bmatrix} \delta_{1} \\ \delta_{2} \\ \vdots \\ \delta_{k} \end{bmatrix} \end{equation*}\]

También, la ecuación (??) supone que cada matriz \(A_i\), \(i = 1, 2, \ldots, p\) está definida de la siguiente forma: \[\begin{equation*} \mathbf{A}_i = \begin{bmatrix} a^{(i)}_{11} & a^{(i)}_{12} & \ldots & a^{(i)}_{1k} \\ a^{(i)}_{21} & a^{(i)}_{22} & \ldots & a^{(i)}_{2k} \\ \vdots & \vdots & \ddots & \vdots \\ a^{(i)}_{k1} & a^{(i)}_{k2} & \ldots & a^{(i)}_{kk} \end{bmatrix} \end{equation*}\]

Donde \(i = 1, 2, \ldots, p\).

Retomando la ecuación (??) y considerando que podemos ocupar el operador rezago \(L^j\) de forma análoga al caso del modelo \(AR(p)\), pero aplicado a un vector, tenemos las siguientes ecuaciones: \[\begin{eqnarray} \mathbf{X}_t - A_1 \mathbf{X}_{t-1} - A_2 \mathbf{X}_{t-2} - \ldots - A_p \mathbf{X}_{t-p} & = & \boldsymbol{\delta} + \mathbf{U}_{t} \nonumber \\ \mathbf{X}_t - A_1 L \mathbf{X}_{t} - A_2 L^2 \mathbf{X}_{t} - \ldots - A_p L^p \mathbf{X}_{t-p} & = & \boldsymbol{\delta} + \mathbf{U}_{t} \nonumber \\ (I_k - \mathbf{A_1} L - \mathbf{A_2} L^2 - \ldots - \mathbf{A_p} L^p) \mathbf{X}_t & = & \boldsymbol{\delta} + \mathbf{U}_{t} \nonumber \\ \mathbf{A}(L) \mathbf{X}_t & = & \boldsymbol{\delta} + \mathbf{U}_{t} \tag{5.1} \end{eqnarray}\]

Adicionalmente, requeriremos que dado que \(\mathbf{U}_t\) es un proceso puramente aleatorio, este debe cumplir con las siguientes condiciones:

El valor esperado del término de error es cero: \[\begin{equation} \mathbb{E}[\mathbf{U}_t] = 0 \end{equation}\]

Existe una matriz de varianzas y covarianzas entre los términos de error contemporáneos dada por: \[\begin{eqnarray} \mathbb{E}[\mathbf{U}_t \mathbf{U}_t'] & = & \mathbb{E} \left[ \begin{bmatrix} U^{(t)}_{1} \\ U^{(t)}_{2} \\ \vdots \\ U^{(t)}_{k} \end{bmatrix} \begin{bmatrix} U^{(t)}_{1} & U^{(t)}_{2} & \ldots & U^{(t)}_{k} \end{bmatrix} \right] \nonumber \\ & = & \mathbb{E} \begin{bmatrix} U^{(t)}_{1} U^{(t)}_{1} & U^{(t)}_{1} U^{(t)}_{2} & \ldots & U^{(t)}_{1} U^{(t)}_{k} \\ U^{(t)}_{2} U^{(t)}_{1} & U^{(t)}_{2} U^{(t)}_{2} & \ldots & U^{(t)}_{2} U^{(t)}_{k} \\ \vdots & \vdots & \ldots & \vdots \\ U^{(t)}_{k} U^{(t)}_{1} & U^{(t)}_{k} U^{(t)}_{2} & \ldots & U^{(t)}_{k} U^{(t)}_{k} \end{bmatrix} \nonumber \\ & = & \begin{bmatrix} \sigma^2_1 & \rho_{12} & \ldots & \rho_{1k} \\ \rho_{21} & \sigma^2_2 & \ldots & \rho_{2k} \\ \vdots & \vdots & \ldots & \vdots \\ \rho_{k1} & \rho_{k2} & \ldots & \sigma^2_k \end{bmatrix} \nonumber \\ & = & \mathbf{\Sigma}_{UU} (\#eq:SigmaVAR) \end{eqnarray}\]

La matriz de varianzas y covarianzas no contemporáneas es nula. Es decir, que para todo \(t \neq s\): \[\begin{eqnarray} \mathbb{E} [\mathbf{U}_t \mathbf{U}_s'] & = & \mathbb{E} \left[ \begin{bmatrix} U^{(t)}_{1} \\ U^{(t)}_{2} \\ \vdots \\ U^{(t)}_{k} \end{bmatrix} \begin{bmatrix} U^{(s)}_{1} & U^{(s)}_{2} & \ldots & U^{(s)}_{k} \end{bmatrix} \right] \nonumber \\ & = & \mathbb{E} \begin{bmatrix} U^{(t)}_{1} U^{(s)}_{1} & U^{(t)}_{1} U^{(s)}_{2} & \ldots & U^{(t)}_{1} U^{(s)}_{k} \\ U^{(t)}_{2} U^{(s)}_{1} & U^{(t)}_{2} U^{(s)}_{2} & \ldots & U^{(t)}_{2} U^{(s)}_{k} \\ \vdots & \vdots & \ldots & \vdots \\ U^{(t)}_{k} U^{(s)}_{1} & U^{(t)}_{k} U^{(s)}_{2} & \ldots & U^{(t)}_{k} U^{(s)}_{k} \end{bmatrix} \nonumber \\ & = & \mathbf{0} (\#eq:RhoVAR) \end{eqnarray}\]

Las ecuaciones (??) y (??) significan que los residuales \(\mathbf{U}_t\) pueden estar correlacionados entre ellos solo en el caso de que la información sea contemporánea, pero no tienen información en común entre residuales de otros periodos.

Al igual que en el caso del modelo o especificación \(AR(p)\) en la especificación del modelo \(VAR(p)\) existen condiciones de estabilidad. Dichas condiciones están dadas por lo siguiente, definamos el siguiente polinomio que resulta de tomar la matriz \(\mathbf{A}(L)\) en la ecuación (5.1): \[\begin{equation} Det[I_t - A_1 z - A_2 z^2 - \ldots - A_p z^p] \neq 0 \end{equation}\]

Donde las raíces del polinomio cumplen que \(|z| \leq 1\), es decir, se ubican dentro del circulo unitario.

La ecuación (5.1) puede ser rexpresada en una forma similar al un proceso de MA. Al respecto, de forma similar a la siguiente ecuación podemos construir un modelo \(VARMA(p,q)\), el cual no estudiamos es este curso.

Reromando el primer planteamiento, podemos escribir: \[\begin{eqnarray} \mathbf{X}_t & = & \mathbf{A}^{-1}(L) \boldsymbol{\delta} + \mathbf{A}^{-1}(L) \mathbf{U}_t \nonumber \\ & = & \boldsymbol{\mu} + \boldsymbol{\beta}(L) \mathbf{U}_t (\#eq:VARMAq) \end{eqnarray}\]

Donde \(\boldsymbol{\mu}\) es un vector de \(k \times 1\) constantes y \(\boldsymbol{\beta}(L)\) es una matriz que depende de \(L\).

Por el lado de las matrices que representan la autocovarianza, estás resultan de resolver lo siguiente: \[\begin{equation} \Gamma_X(\tau) = E[(\mathbf{X}_t - \mu)(\mathbf{X}_{t-\tau} - \mu)'] \end{equation}\]

Ahora, sin pérdida de generalidad digamos que la especificación VAR(p) en la ecuación (??) no tiene constante, por lo que \(\boldsymbol{\delta} = \mathbf{0}\), lo que implica que \(\boldsymbol{\mu} = \mathbf{0}\). De esta forma las matrices de autocovarianza resultan de: \[\begin{eqnarray*} \Gamma_{\mathbf{X}}(\tau) & = & E[(\mathbf{X}_t)(\mathbf{X}_{t-\tau})'] \\ & = & \mathbf{A_1} E[(\mathbf{X}_{t-1})(\mathbf{X}_{t-\tau})'] + \mathbf{A_2} E[(\mathbf{X}_{t-2})(\mathbf{X}_{t-\tau})'] \\ & & + \ldots + \mathbf{A_p} E[(\mathbf{X}_{t-p})(\mathbf{X}_{t-\tau})'] + E[(\mathbf{U}_t(\mathbf{X}_{t-\tau})'] \end{eqnarray*}\]

Finalmente, al igual que en el caso \(AR(p)\), requerimos de una métrica que nos permita determinar el número de rezagos óptimo \(p\) en el \(VAR(p)\). Así, establecemos criterios de información similares a los del \(AR(p)\) dados por:

1.Final Prediction Error (FPE): \[\begin{equation} FPE(p) = \left[ \frac{T + kp + 1}{T - kp - 1} \right]^k |\mathbf{\Sigma}_{\hat{U}\hat{U}}(p)| \end{equation}\]

Akaike Criterion (AIC): \[\begin{equation} AIC(p) = ln|\mathbf{\Sigma}_{\hat{U}\hat{U}}(p)| + (k + p k^2) \frac{2}{T} \end{equation}\]

Hannan - Quinn Criterion (HQ): \[\begin{equation} HQ(p) = ln|\mathbf{\Sigma}_{\hat{U}\hat{U}}(p)| + (k + p k^2) \frac{2ln(ln(2))}{T} \end{equation}\]

Schwartz Criterion (SC): \[\begin{equation} SC(p) = ln|\mathbf{\Sigma}_{\hat{U}\hat{U}}(p)| + (k + p k^2) \frac{ln(T)}{T} \end{equation}\]

Donde la matriz de varianzas y covarianzas contemporáneas estará dada por: \[\begin{equation*} \mathbf{\Sigma}_{\hat{U}\hat{U}}(p) = \mathbb{E} \left[ \begin{bmatrix} U^{(t)}_{1} \\ U^{(t)}_{2} \\ \vdots \\ U^{(t)}_{k} \end{bmatrix} \begin{bmatrix} U^{(t)}_{1} & U^{(t)}_{2} & \ldots & U^{(t)}_{k} \end{bmatrix} \right] \end{equation*}\]

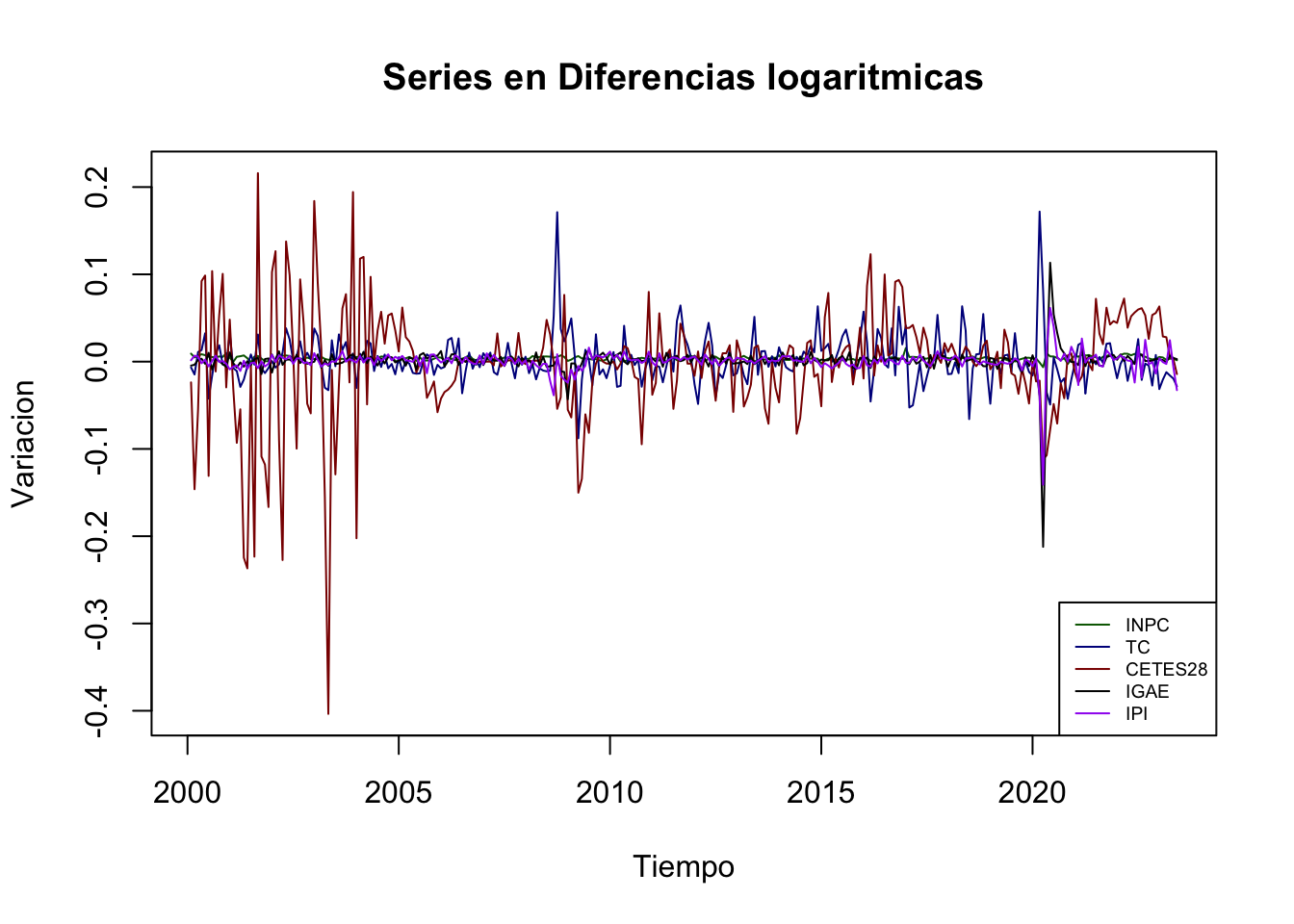

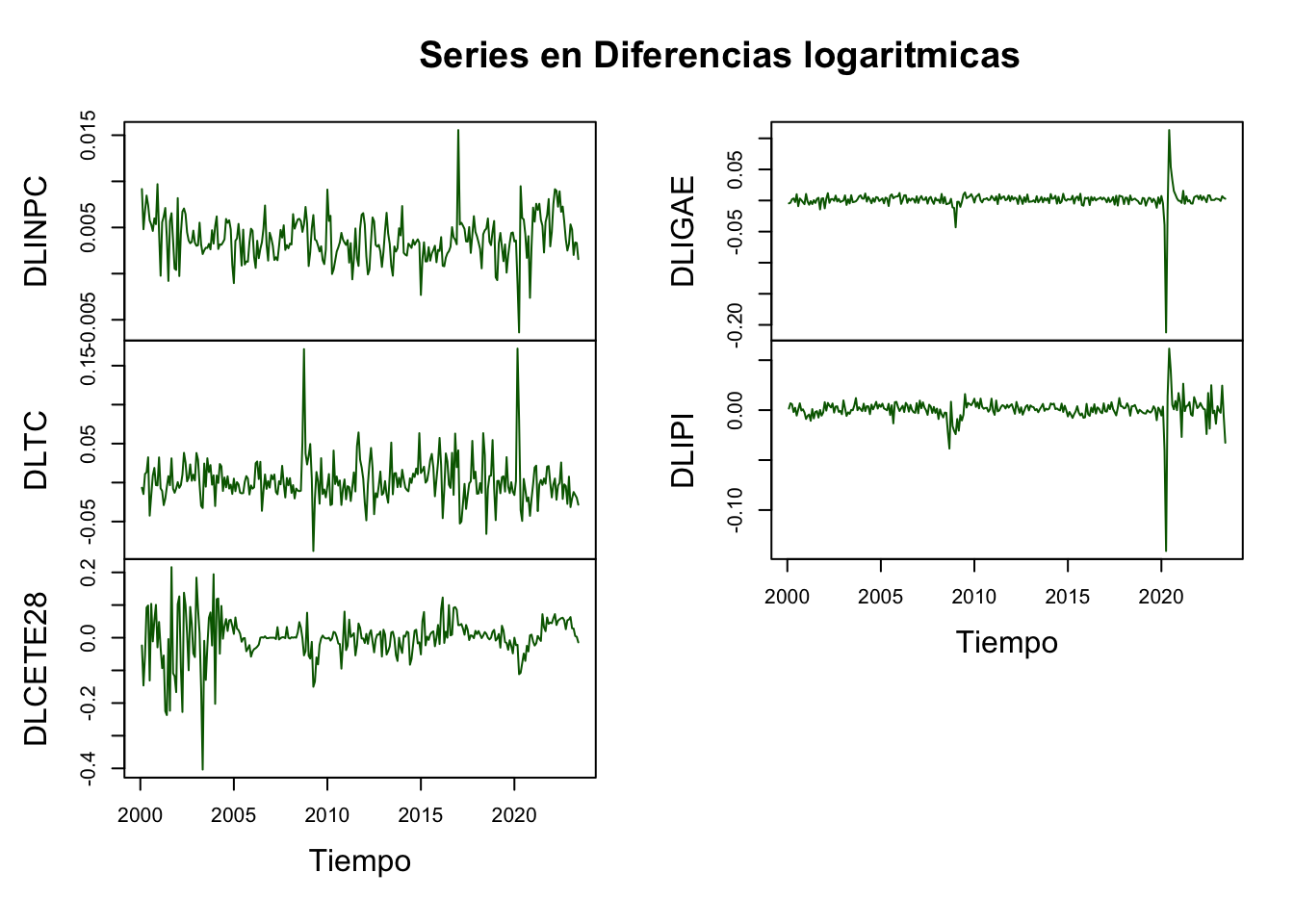

. Ahora veámos un ejemplo de estimación de \(VAR(p)\). Para el ejemplo utilizaremos las series de INPC, Tipo de Cambio, rendimiento de los Cetes a 28 días, el IGAE y el Índice de Producción Industrial de los Estados Unidos, todas desestacionalizadas y para el período de enero de 2000 a julio de 2019. Dado que el supuesto estacionariedad sigue presente en nuestro análisis, emplearemos cada una de las series en su versión de diferencias logaritmicas. Las Figuras 5.2 y 5.3 muestra las series referidas.

library(ggplot2)

library(dplyr)

library(stats)

library(MASS)

library(strucchange)

library(zoo)

library(sandwich)

library(urca)

library(lmtest)

library(vars)

#

load("BD/Datos_Ad.RData")

#

DLINPC <- diff(log( ts(Datos_Ad$INPC_Ad, start = c(2000, 1), freq = 12) ))

DLTC <- diff(log( ts(Datos_Ad$TC_Ad, start = c(2000, 1), freq = 12) ))

DLCETE28 <- diff(log( ts(Datos_Ad$CETE28_Ad, start = c(2000, 1), freq = 12) ))

DLIGAE <- diff(log( ts(Datos_Ad$IGAE_Ad, start = c(2000, 1), freq = 12) ))

DLIPI <- diff(log( ts(Datos_Ad$IPI_Ad, start = c(2000, 1), freq = 12) ))

Datos <- data.frame(cbind(DLINPC, DLTC, DLCETE28, DLIGAE, DLIPI))

Datos <- ts(Datos,

start = c(2000, 2), freq = 12)plot(Datos, plot.type = "s",

col = c("darkgreen", "darkblue", "darkred", "black", "purple"),

main = "Series en Diferencias logaritmicas",

xlab = "Tiempo", ylab = "Variacion")

legend("bottomright", c("INPC", "TC", "CETES28", "IGAE", "IPI"),

cex = 0.6, lty = 1:1,

col = c("darkgreen", "darkblue", "darkred", "black", "purple"))

Figure 5.2: Series en diferencias logarítmicas (Forma 1)

plot(Datos, plot.type = "m",

col = "darkgreen",

main = "Series en Diferencias logaritmicas", xlab = "Tiempo")

Figure 5.3: Series en diferencias logarítmicas (Forma 2)

Dicho lo anterior, a continuación mostraremos la tabla que resume el valor de los distintos criterios de información para una especificación de un \(VAR(p)\) con constante. Notése que es posible especificar un \(VAR(p)\) con tendencia, siempre que exista evidencia de que algunas de las series sean estacionarias alrededor de una tendencia. Caso que no aplica hasta este momento, ya que nuestro análisis de estacionariedad es claro respecto a la media constante (más adelante aportaremos la evidencia de esto), lo cual elimina la posibilidad de incluir una tendencia.

En el Cuadro 5.2 reportamos el número de rezagos propuesto a partir de cada criterio de información y en el Cuadro 5.3 reportamos los resultados de aplicar una prueba de criterios de información para diferentes valores de rezagos. Del cual se concluye que el número óptimo de rezagos es 2 (según el criterio AIC y el FPE) y 1 (según el criterio HQ y el SC). Recordemos que es común que el criterio AIC siempre reporte el mayor valor de rezagos, por lo que es una buena práctica utilizarlo como referente principal.

| AIC | HQ | SC | FPE |

|---|---|---|---|

| 2 | 1 | 1 | 2 |

| Rezagos | AIC | HQ | SC | FPE |

|---|---|---|---|---|

| 1 | -4.636412e+01 | -4.617847e+01 | -4.590430e+01 | 7.317262e-21 |

| 2 | -4.639541e+01 | -4.605506e+01 | -4.555241e+01 | 7.094216e-21 |

| 3 | -4.635305e+01 | -4.585799e+01 | -4.512686e+01 | 7.407479e-21 |

| \(\vdots\) | \(\vdots\) | \(\vdots\) | \(\vdots\) | \(\vdots\) |

## $selection

## AIC(n) HQ(n) SC(n) FPE(n)

## 2 1 1 2

##

## $criteria

## 1 2 3 4 5

## AIC(n) -4.343694e+01 -4.348783e+01 -4.342685e+01 -4.338688e+01 -4.329316e+01

## HQ(n) -4.327594e+01 -4.319266e+01 -4.299751e+01 -4.282338e+01 -4.259549e+01

## SC(n) -4.303604e+01 -4.275285e+01 -4.235779e+01 -4.198374e+01 -4.155594e+01

## FPE(n) 1.366449e-19 1.298899e-19 1.381225e-19 1.438821e-19 1.582460e-19

## 6 7 8 9 10

## AIC(n) -4.324317e+01 -4.329021e+01 -4.324194e+01 -4.322014e+01 -4.317881e+01

## HQ(n) -4.241133e+01 -4.232420e+01 -4.214176e+01 -4.198580e+01 -4.181030e+01

## SC(n) -4.117187e+01 -4.088482e+01 -4.050247e+01 -4.014660e+01 -3.977118e+01

## FPE(n) 1.667106e-19 1.595179e-19 1.680601e-19 1.726236e-19 1.810365e-19

## 11 12

## AIC(n) -4.311914e+01 -4.305022e+01

## HQ(n) -4.161646e+01 -4.141338e+01

## SC(n) -3.937743e+01 -3.897444e+01

## FPE(n) 1.936459e-19 2.093856e-19De esta forma, justificamos la estimación de un \(VAR(2)\). Los resultados del mismo se reportan en los siguientes cuadros, en los que se muestra el resultado de una de las ecuaciones. Los resultados restantes se encuentran en el código de R mostrado más abajo. Primero mostraremos los resultados de las raíces del polinomio característico en el Cuadro 5.4, seguido de un cuadro para la ecuación del IGAE en el Cuadro 5.5 (por simplicidad se omiten las otras cuatro ecuaciones del VAR(2)), y del Cuadro 5.6 con la matriz \(\mathbf{\Sigma}_{\hat{U}\hat{U}}\) estimada del VAR.

| 0.7452 | 0.4403 | 0.4403 | 0.3503 | 0.3503 |

| 0.3342 | 0.3342 | 0.3339 | 0.3339 | 0.06951 |

| Variable | Coeficiente | Error Est. | Estad. t | Prob.(\(>\) t) |

|---|---|---|---|---|

| \(DLINPC_{t-1}\) | -0.2584978 | 0.1658396 | -1.559 | 0.120493 |

| \(DLTC_{t-1}\) | 0.0022016 | 0.0152876 | 0.144 | 0.885620 |

| \(DLCETE28_{t-1}\) | 0.0009547 | 0.0049115 | 0.194 | 0.846054 |

| \(DLIGAE_{t-1}\) | -0.2351453 | 0.0699797 | -3.360 | 0.000917 *** |

| \(DLIPI_{t-1}\) | 0.2442406 | 0.0600502 | 4.067 | 6.62e-05 *** |

| \(DLINPC_{t-2}\) | -0.0775039 | 0.1694809 | -0.457 | 0.647904 |

| \(DLTC_{t-2}\) | -0.0413316 | 0.0144650 | -2.857 | 0.004680 ** |

| \(DLCETE28_{t-2}\) | 0.0005341 | 0.0048058 | 0.111 | 0.911612 |

| \(DLIGAE_{t-2}\) | -0.0646890 | 0.0693711 | -0.933 | 0.352092 |

| \(DLIPI_{t-2}\) | 0.1796286 | 0.0620861 | 2.893 | 0.004195 ** |

| \(\delta_4\) | 0.0030377 | 0.0008077 | 3.761 | 0.000217 *** |

| Notas: | *** | signif. | al 0.1% | |

| ** | signif. | al 1% | ||

| * | signif. | al 5% |

| \(DLINPC_t\) | \(DLTC_t\) | \(DLCE28_t\) | \(DLIGAE_t\) | \(DLIGAE_t\) | |

| \(DLINPC_t\) | 3.95e-06 | 3.19e-06 | -1.83e-06 | -5.29-07 | 1.34e-06 |

| \(DLTC_t\) | 3.19e-06 | 5.04e-04 | 4.27e-04 | 9.81e-06 | 1.61e-05 |

| \(DLCE28_t\) | -1.83e-06 | 4.27e-04 | 4.63e-03 | 1.26e-05 | 2.76e-05 |

| \(DLIGAE_t\) | -5.29e-07 | 9.81e-06 | 1.26e-05 | 2.43e-05 | 8.75e-06 |

| \(DLIGAE_t\) | 1.34e-06 | 1.61e-05 | 2.76e-05 | 8.75e-06 | 3.13e-05 |

##

## VAR Estimation Results:

## =========================

## Endogenous variables: DLINPC, DLTC, DLCETE28, DLIGAE, DLIPI

## Deterministic variables: const

## Sample size: 279

## Log Likelihood: 4142.895

## Roots of the characteristic polynomial:

## 0.53 0.53 0.4501 0.4501 0.4425 0.4425 0.3251 0.3251 0.1677 0.1677

## Call:

## VAR(y = Datos, p = 2, type = "const")

##

##

## Estimation results for equation DLINPC:

## =======================================

## DLINPC = DLINPC.l1 + DLTC.l1 + DLCETE28.l1 + DLIGAE.l1 + DLIPI.l1 + DLINPC.l2 + DLTC.l2 + DLCETE28.l2 + DLIGAE.l2 + DLIPI.l2 + const

##

## Estimate Std. Error t value Pr(>|t|)

## DLINPC.l1 0.387061 0.063100 6.134 3.06e-09 ***

## DLTC.l1 -0.004611 0.005286 -0.872 0.3839

## DLCETE28.l1 0.001229 0.002078 0.592 0.5546

## DLIGAE.l1 -0.022088 0.015077 -1.465 0.1441

## DLIPI.l1 0.009878 0.019363 0.510 0.6104

## DLINPC.l2 -0.006707 0.063621 -0.105 0.9161

## DLTC.l2 0.009608 0.005496 1.748 0.0816 .

## DLCETE28.l2 0.001827 0.002051 0.891 0.3737

## DLIGAE.l2 0.006544 0.014289 0.458 0.6473

## DLIPI.l2 -0.015245 0.019632 -0.777 0.4381

## const 0.002325 0.000294 7.908 6.88e-14 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

##

## Residual standard error: 0.002176 on 268 degrees of freedom

## Multiple R-Squared: 0.1783, Adjusted R-squared: 0.1476

## F-statistic: 5.815 on 10 and 268 DF, p-value: 6.289e-08

##

##

## Estimation results for equation DLTC:

## =====================================

## DLTC = DLINPC.l1 + DLTC.l1 + DLCETE28.l1 + DLIGAE.l1 + DLIPI.l1 + DLINPC.l2 + DLTC.l2 + DLCETE28.l2 + DLIGAE.l2 + DLIPI.l2 + const

##

## Estimate Std. Error t value Pr(>|t|)

## DLINPC.l1 -1.344803 0.745382 -1.804 0.07233 .

## DLTC.l1 0.315786 0.062442 5.057 7.9e-07 ***

## DLCETE28.l1 -0.039912 0.024542 -1.626 0.10506

## DLIGAE.l1 0.379306 0.178102 2.130 0.03411 *

## DLIPI.l1 -0.514827 0.228727 -2.251 0.02521 *

## DLINPC.l2 0.071779 0.751538 0.096 0.92398

## DLTC.l2 -0.183813 0.064926 -2.831 0.00499 **

## DLCETE28.l2 0.030125 0.024228 1.243 0.21481

## DLIGAE.l2 0.070713 0.168797 0.419 0.67561

## DLIPI.l2 -0.166610 0.231909 -0.718 0.47312

## const 0.006463 0.003473 1.861 0.06388 .

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

##

## Residual standard error: 0.0257 on 268 degrees of freedom

## Multiple R-Squared: 0.1425, Adjusted R-squared: 0.1105

## F-statistic: 4.454 on 10 and 268 DF, p-value: 8.102e-06

##

##

## Estimation results for equation DLCETE28:

## =========================================

## DLCETE28 = DLINPC.l1 + DLTC.l1 + DLCETE28.l1 + DLIGAE.l1 + DLIPI.l1 + DLINPC.l2 + DLTC.l2 + DLCETE28.l2 + DLIGAE.l2 + DLIPI.l2 + const

##

## Estimate Std. Error t value Pr(>|t|)

## DLINPC.l1 3.933798 1.861561 2.113 0.0355 *

## DLTC.l1 0.112997 0.155945 0.725 0.4693

## DLCETE28.l1 0.113300 0.061292 1.849 0.0656 .

## DLIGAE.l1 -0.588758 0.444803 -1.324 0.1868

## DLIPI.l1 1.174496 0.571237 2.056 0.0407 *

## DLINPC.l2 -2.213087 1.876936 -1.179 0.2394

## DLTC.l2 0.117661 0.162151 0.726 0.4687

## DLCETE28.l2 0.063398 0.060509 1.048 0.2957

## DLIGAE.l2 -0.237974 0.421565 -0.565 0.5729

## DLIPI.l2 1.110203 0.579183 1.917 0.0563 .

## const -0.007514 0.008674 -0.866 0.3872

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

##

## Residual standard error: 0.06419 on 268 degrees of freedom

## Multiple R-Squared: 0.08823, Adjusted R-squared: 0.05421

## F-statistic: 2.593 on 10 and 268 DF, p-value: 0.005122

##

##

## Estimation results for equation DLIGAE:

## =======================================

## DLIGAE = DLINPC.l1 + DLTC.l1 + DLCETE28.l1 + DLIGAE.l1 + DLIPI.l1 + DLINPC.l2 + DLTC.l2 + DLCETE28.l2 + DLIGAE.l2 + DLIPI.l2 + const

##

## Estimate Std. Error t value Pr(>|t|)

## DLINPC.l1 0.719855 0.393617 1.829 0.0685 .

## DLTC.l1 -0.218508 0.032974 -6.627 1.88e-10 ***

## DLCETE28.l1 0.007718 0.012960 0.596 0.5520

## DLIGAE.l1 0.037559 0.094051 0.399 0.6900

## DLIPI.l1 0.389894 0.120785 3.228 0.0014 **

## DLINPC.l2 -0.737653 0.396868 -1.859 0.0642 .

## DLTC.l2 0.073830 0.034286 2.153 0.0322 *

## DLCETE28.l2 -0.013542 0.012794 -1.058 0.2908

## DLIGAE.l2 -0.142845 0.089138 -1.603 0.1102

## DLIPI.l2 -0.154835 0.122465 -1.264 0.2072

## const 0.001637 0.001834 0.893 0.3729

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

##

## Residual standard error: 0.01357 on 268 degrees of freedom

## Multiple R-Squared: 0.3272, Adjusted R-squared: 0.3021

## F-statistic: 13.03 on 10 and 268 DF, p-value: < 2.2e-16

##

##

## Estimation results for equation DLIPI:

## ======================================

## DLIPI = DLINPC.l1 + DLTC.l1 + DLCETE28.l1 + DLIGAE.l1 + DLIPI.l1 + DLINPC.l2 + DLTC.l2 + DLCETE28.l2 + DLIGAE.l2 + DLIPI.l2 + const

##

## Estimate Std. Error t value Pr(>|t|)

## DLINPC.l1 0.042383 0.326611 0.130 0.8968

## DLTC.l1 -0.163742 0.027361 -5.985 6.93e-09 ***

## DLCETE28.l1 0.012143 0.010754 1.129 0.2598

## DLIGAE.l1 0.098821 0.078041 1.266 0.2065

## DLIPI.l1 0.067742 0.100224 0.676 0.4997

## DLINPC.l2 -0.524835 0.329309 -1.594 0.1122

## DLTC.l2 0.053353 0.028449 1.875 0.0618 .

## DLCETE28.l2 -0.016237 0.010616 -1.529 0.1273

## DLIGAE.l2 -0.088483 0.073964 -1.196 0.2326

## DLIPI.l2 -0.082982 0.101618 -0.817 0.4149

## const 0.002361 0.001522 1.551 0.1220

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

##

## Residual standard error: 0.01126 on 268 degrees of freedom

## Multiple R-Squared: 0.1978, Adjusted R-squared: 0.1679

## F-statistic: 6.61 on 10 and 268 DF, p-value: 3.715e-09

##

##

##

## Covariance matrix of residuals:

## DLINPC DLTC DLCETE28 DLIGAE DLIPI

## DLINPC 4.735e-06 -1.939e-07 4.559e-06 6.652e-06 7.000e-06

## DLTC -1.939e-07 6.607e-04 3.698e-04 -3.544e-05 -3.174e-05

## DLCETE28 4.559e-06 3.698e-04 4.121e-03 6.362e-05 8.525e-05

## DLIGAE 6.652e-06 -3.544e-05 6.362e-05 1.842e-04 1.164e-04

## DLIPI 7.000e-06 -3.174e-05 8.525e-05 1.164e-04 1.268e-04

##

## Correlation matrix of residuals:

## DLINPC DLTC DLCETE28 DLIGAE DLIPI

## DLINPC 1.000000 -0.003466 0.03264 0.22524 0.2856

## DLTC -0.003466 1.000000 0.22409 -0.10159 -0.1097

## DLCETE28 0.032640 0.224095 1.00000 0.07301 0.1179

## DLIGAE 0.225240 -0.101585 0.07301 1.00000 0.7615

## DLIPI 0.285629 -0.109656 0.11792 0.76147 1.0000Finalmente, en el Cuadro 5.7 reportamos las pruebas de diagnóstico del VAR(2). Incluimos las pruebas de correlación serial (o autocorrelación), normalidad y de heterocedasticidad. De acuerdo con esa información, la correlación serial muestra que existe relación de la matriz de covarianzas no contemporánea considerando pocos rezagos, pero se elimina conforme los rezagos se incrementan. En cuanto a normalidad, se observa que los residuales no lo son, por lo que se requeriría mejorar la especificación del VAR. Finalmente, se observa que los residuales no son homocedásticos.

| Estadística (rezagos) | Coeficiente | p-value | Conclusión |

|---|---|---|---|

| Correlación Serial (\(\chi^2 (2)\)) | 59.436 | 0.1696 | Existe autocorrelación serial |

| Correlación Serial (\(\chi^2 (4)\)) | 127.17 | 0.03461 | No existe autocorrelación serial |

| Correlación Serial (\(\chi^2 (6)\)) | 183.14 | 0.03393 | No existe autocorrelación serial |

| Normalidad - JB (\(\chi^2\)) | 2335 | 0.0000 | Los residuales no son normales |

| ARCH (\(\chi^2 (2)\)) | 691.58 | 0.0000 | Los residuales no son homocedásticos |

## $JB

##

## JB-Test (multivariate)

##

## data: Residuals of VAR object VAR_p

## Chi-squared = 36186, df = 10, p-value < 2.2e-16

##

##

## $Skewness

##

## Skewness only (multivariate)

##

## data: Residuals of VAR object VAR_p

## Chi-squared = 1261, df = 5, p-value < 2.2e-16

##

##

## $Kurtosis

##

## Kurtosis only (multivariate)

##

## data: Residuals of VAR object VAR_p

## Chi-squared = 34925, df = 5, p-value < 2.2e-16##

## Breusch-Godfrey LM test

##

## data: Residuals of VAR object VAR_p

## Chi-squared = 74.839, df = 50, p-value = 0.013##

## Breusch-Godfrey LM test

##

## data: Residuals of VAR object VAR_p

## Chi-squared = 131.69, df = 100, p-value = 0.01849##

## Breusch-Godfrey LM test

##

## data: Residuals of VAR object VAR_p

## Chi-squared = 201.63, df = 150, p-value = 0.003147##

## ARCH (multivariate)

##

## data: Residuals of VAR object VAR_p

## Chi-squared = 2122.4, df = 1350, p-value < 2.2e-165.3 Análisis de Impulso-Respuesta

Una de las grandes ventajas que aporta el análisis de los modelos VAR es el análisis de Impulso-Respuesta. Dicho análisis busca cuantificar el efecto que tiene en \(\mathbf{X}_t\) una innovación o cambio en los residuales de cualquiera de las variables en un momento definido. Partamos de la ecuación (??) de forma que tenemos: \[\begin{eqnarray} \mathbf{X}_t & = & \mathbf{A}^{-1}(L) \delta + \mathbf{A}^{-1}(L) \mathbf{U}_t \nonumber \\ & = & \mu + \mathbf{B}(L) \mathbf{U}_t \nonumber \\ & = & \mu + \Psi_0 \mathbf{U}_t + \Psi_1 \mathbf{U}_{t-1} + \Psi_2 \mathbf{U}_{t-2} + \Psi_3 \mathbf{U}_{t-3} + \ldots \end{eqnarray}\]

Donde \(\Psi_0 = I\) y cada una de las \(\Psi_i = - \mathbf{B}_i\), \(i = 1, 2, \ldots\). De esta forma se verifica el efecto que tiene en \(\mathbf{X}_t\) cada una de las innovaciones pasadas. Por lo que el análisis de Impulso-Respuesta cuantifica el efecto de cada una de esas matrices en las que hemos descompuesto a \(\mathbf{B}(L)\).

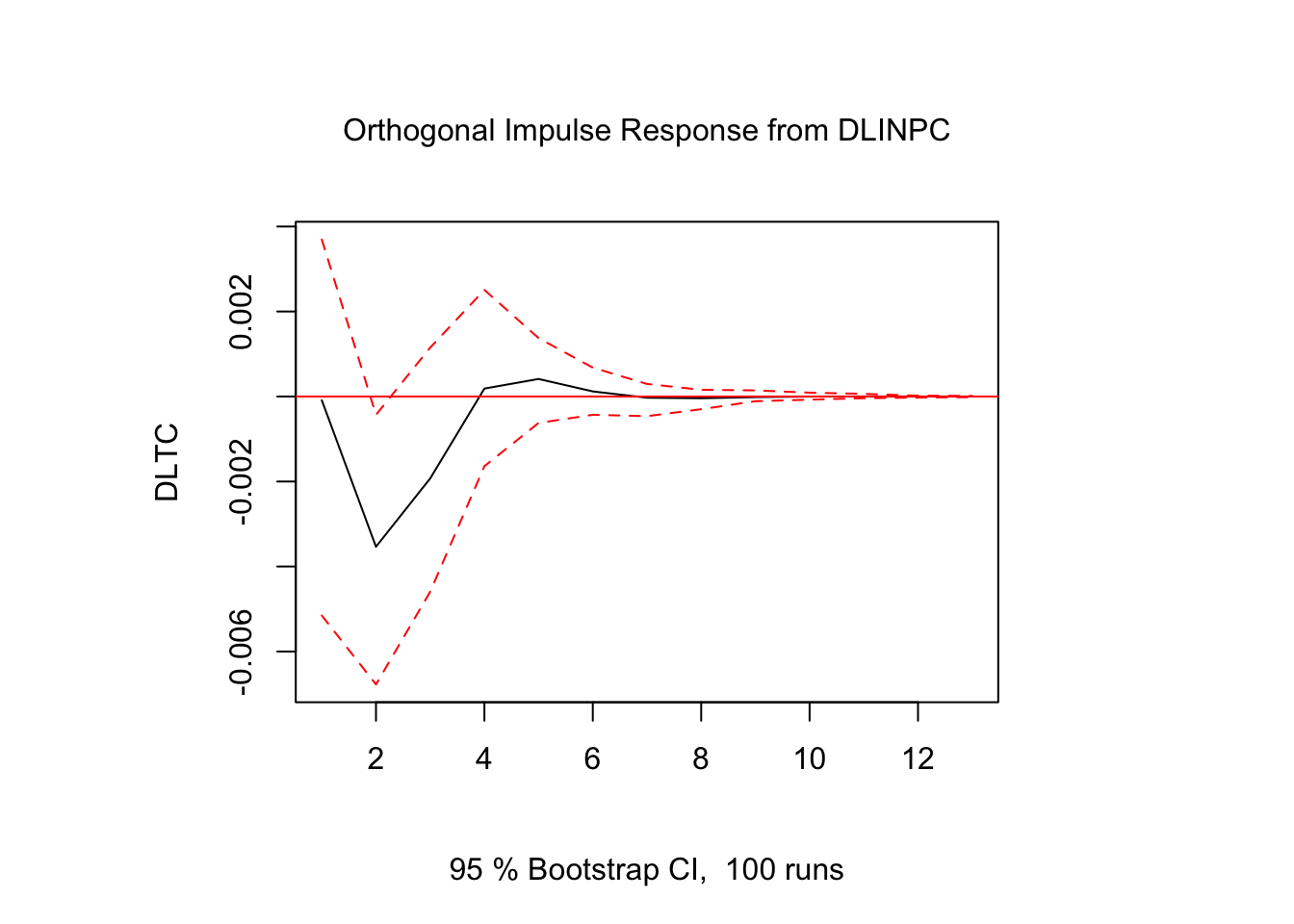

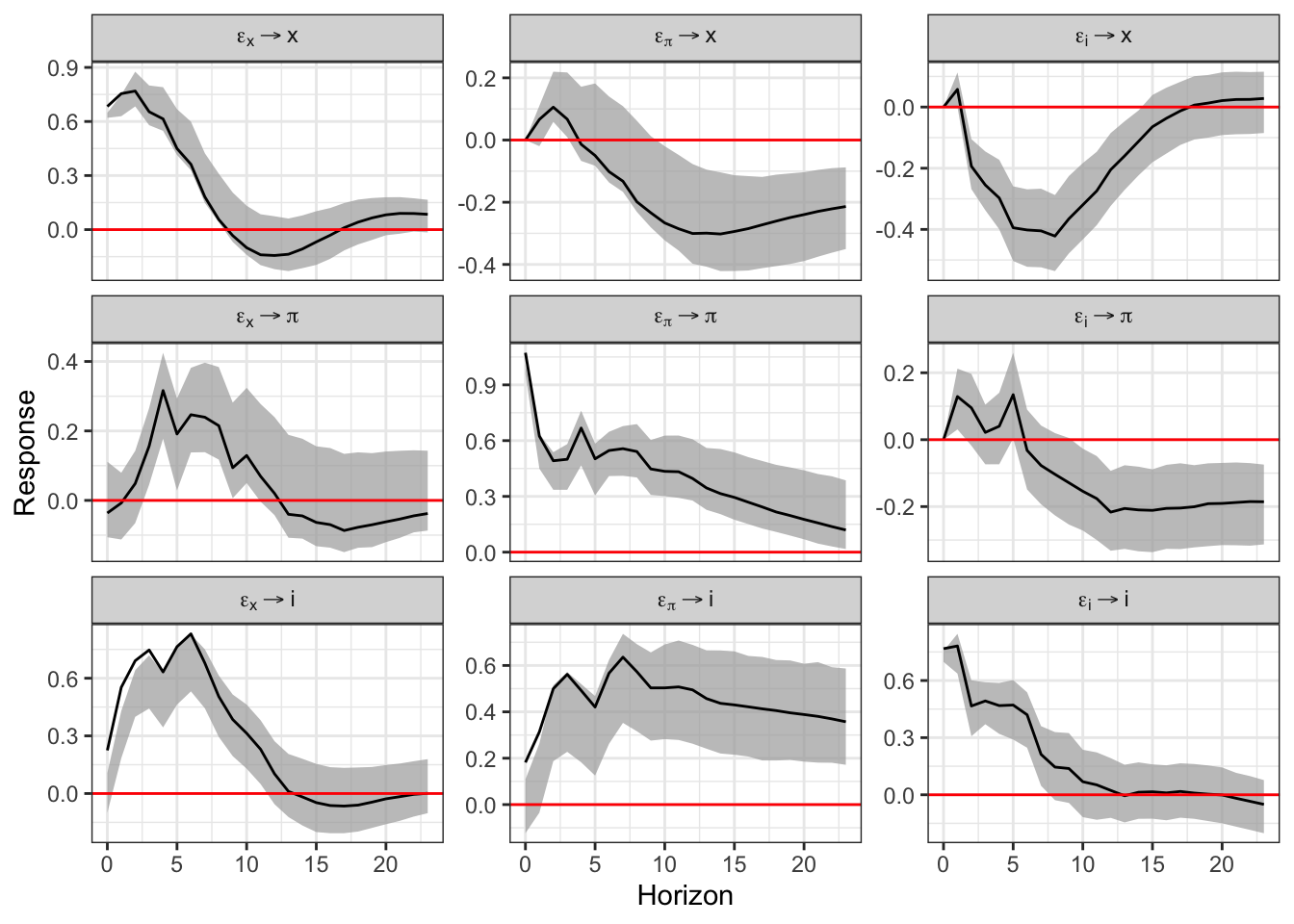

. Retomando el modelo \(VAR(2)\) anteriormente estimado, en las siguientes figuras reportamos las gráficas de Impulso-Respuesta de la serie \(DLTC_t\) ante cambios en los residuales del resto de las series y de la propia serie.

##

## Impulse response coefficients

## $DLINPC

## DLINPC

## [1,] 2.175900e-03

## [2,] 8.094393e-04

## [3,] 2.429936e-04

## [4,] 1.049000e-04

## [5,] 4.305193e-05

## [6,] 2.571953e-05

## [7,] 1.084055e-05

## [8,] 1.147158e-06

## [9,] -1.425663e-06

## [10,] -9.999499e-07

## [11,] -3.443770e-07

## [12,] -1.512886e-07

## [13,] -1.157354e-07

##

## $DLTC

## DLINPC

## [1,] 0.000000e+00

## [2,] -8.268371e-05

## [3,] 3.117547e-04

## [4,] 2.648975e-04

## [5,] 5.871629e-05

## [6,] -2.894914e-05

## [7,] -1.054637e-05

## [8,] 1.057859e-05

## [9,] 7.621634e-06

## [10,] -4.038885e-07

## [11,] -2.113820e-06

## [12,] -4.691794e-07

## [13,] 3.771599e-07

##

## $DLCETE28

## DLINPC

## [1,] 0.000000e+00

## [2,] 6.486929e-05

## [3,] 1.318264e-04

## [4,] 3.487944e-05

## [5,] 4.740702e-05

## [6,] 3.336371e-05

## [7,] 1.571610e-05

## [8,] 3.770470e-06

## [9,] 5.672766e-08

## [10,] 2.556950e-07

## [11,] 3.379406e-07

## [12,] 4.626880e-08

## [13,] -1.137662e-07

##

## $DLIGAE

## DLINPC

## [1,] 0.000000e+00

## [2,] -2.115678e-04

## [3,] -1.790075e-04

## [4,] -1.453804e-05

## [5,] 4.387550e-05

## [6,] 1.348413e-05

## [7,] -6.605412e-06

## [8,] -3.449275e-06

## [9,] 2.238652e-06

## [10,] 2.066817e-06

## [11,] 8.258756e-08

## [12,] -4.659518e-07

## [13,] -9.698431e-08

##

## $DLIPI

## DLINPC

## [1,] 0.000000e+00

## [2,] 7.038188e-05

## [3,] -1.107780e-04

## [4,] -3.218008e-05

## [5,] -1.697303e-05

## [6,] 4.856595e-07

## [7,] 1.045292e-05

## [8,] 4.695418e-06

## [9,] 3.599640e-07

## [10,] -5.104865e-07

## [11,] 5.294854e-08

## [12,] 2.664766e-07

## [13,] 9.015073e-08

##

##

## Lower Band, CI= 0.95

## $DLINPC

## DLINPC

## [1,] 1.856243e-03

## [2,] 5.338466e-04

## [3,] 1.145367e-05

## [4,] -6.189318e-05

## [5,] -6.627741e-05

## [6,] -4.974017e-05

## [7,] -2.673701e-05

## [8,] -1.727988e-05

## [9,] -1.143222e-05

## [10,] -8.985796e-06

## [11,] -3.902849e-06

## [12,] -2.045231e-06

## [13,] -9.437671e-07

##

## $DLTC

## DLINPC

## [1,] 0.000000e+00

## [2,] -3.539885e-04

## [3,] 1.070428e-05

## [4,] 8.629234e-05

## [5,] -4.215293e-05

## [6,] -9.197116e-05

## [7,] -7.834160e-05

## [8,] -1.329314e-05

## [9,] -3.726249e-06

## [10,] -1.178555e-05

## [11,] -6.632017e-06

## [12,] -6.610783e-06

## [13,] -4.530480e-06

##

## $DLCETE28

## DLINPC

## [1,] 0.000000e+00

## [2,] -1.918576e-04

## [3,] -1.816116e-04

## [4,] -1.023272e-04

## [5,] -5.242507e-05

## [6,] -1.726171e-05

## [7,] -7.256438e-06

## [8,] -9.136482e-06

## [9,] -1.113404e-05

## [10,] -4.792317e-06

## [11,] -3.266766e-06

## [12,] -2.092713e-06

## [13,] -8.422396e-07

##

## $DLIGAE

## DLINPC

## [1,] 0.000000e+00

## [2,] -3.950775e-04

## [3,] -3.818985e-04

## [4,] -1.521840e-04

## [5,] -3.300378e-05

## [6,] -4.654161e-05

## [7,] -3.714319e-05

## [8,] -2.402101e-05

## [9,] -1.385246e-05

## [10,] -5.043412e-06

## [11,] -5.510753e-06

## [12,] -3.499269e-06

## [13,] -2.092795e-06

##

## $DLIPI

## DLINPC

## [1,] 0.000000e+00

## [2,] -1.837313e-04

## [3,] -3.716721e-04

## [4,] -1.282491e-04

## [5,] -1.318774e-04

## [6,] -6.095915e-05

## [7,] -9.151907e-06

## [8,] -6.150211e-06

## [9,] -7.626032e-06

## [10,] -1.065900e-05

## [11,] -7.526565e-06

## [12,] -1.810036e-06

## [13,] -1.263063e-06

##

##

## Upper Band, CI= 0.95

## $DLINPC

## DLINPC

## [1,] 2.412128e-03

## [2,] 1.023698e-03

## [3,] 5.055812e-04

## [4,] 2.393350e-04

## [5,] 1.466108e-04

## [6,] 1.048481e-04

## [7,] 6.326779e-05

## [8,] 3.676095e-05

## [9,] 1.995589e-05

## [10,] 1.199759e-05

## [11,] 6.384238e-06

## [12,] 5.172229e-06

## [13,] 3.379666e-06

##

## $DLTC

## DLINPC

## [1,] 0.000000e+00

## [2,] 2.275848e-04

## [3,] 5.209623e-04

## [4,] 3.963001e-04

## [5,] 1.693697e-04

## [6,] 3.570633e-05

## [7,] 3.731144e-05

## [8,] 3.930504e-05

## [9,] 3.051177e-05

## [10,] 2.045376e-05

## [11,] 5.830627e-06

## [12,] 5.543261e-06

## [13,] 2.689511e-06

##

## $DLCETE28

## DLINPC

## [1,] 0.000000e+00

## [2,] 2.638020e-04

## [3,] 3.955110e-04

## [4,] 1.818647e-04

## [5,] 1.461015e-04

## [6,] 8.546904e-05

## [7,] 4.583759e-05

## [8,] 1.770772e-05

## [9,] 9.420025e-06

## [10,] 6.621940e-06

## [11,] 4.034500e-06

## [12,] 2.222779e-06

## [13,] 1.232539e-06

##

## $DLIGAE

## DLINPC

## [1,] 0.000000e+00

## [2,] 4.755774e-05

## [3,] 4.721739e-05

## [4,] 8.729862e-05

## [5,] 1.255336e-04

## [6,] 6.442026e-05

## [7,] 1.967899e-05

## [8,] 1.129316e-05

## [9,] 1.358591e-05

## [10,] 8.569580e-06

## [11,] 5.095150e-06

## [12,] 3.332386e-06

## [13,] 1.930672e-06

##

## $DLIPI

## DLINPC

## [1,] 0.000000e+00

## [2,] 3.057004e-04

## [3,] 1.463766e-04

## [4,] 8.715319e-05

## [5,] 8.869526e-05

## [6,] 4.525828e-05

## [7,] 3.695326e-05

## [8,] 2.340300e-05

## [9,] 6.902277e-06

## [10,] 3.022663e-06

## [11,] 1.657242e-06

## [12,] 2.107922e-06

## [13,] 1.960968e-06

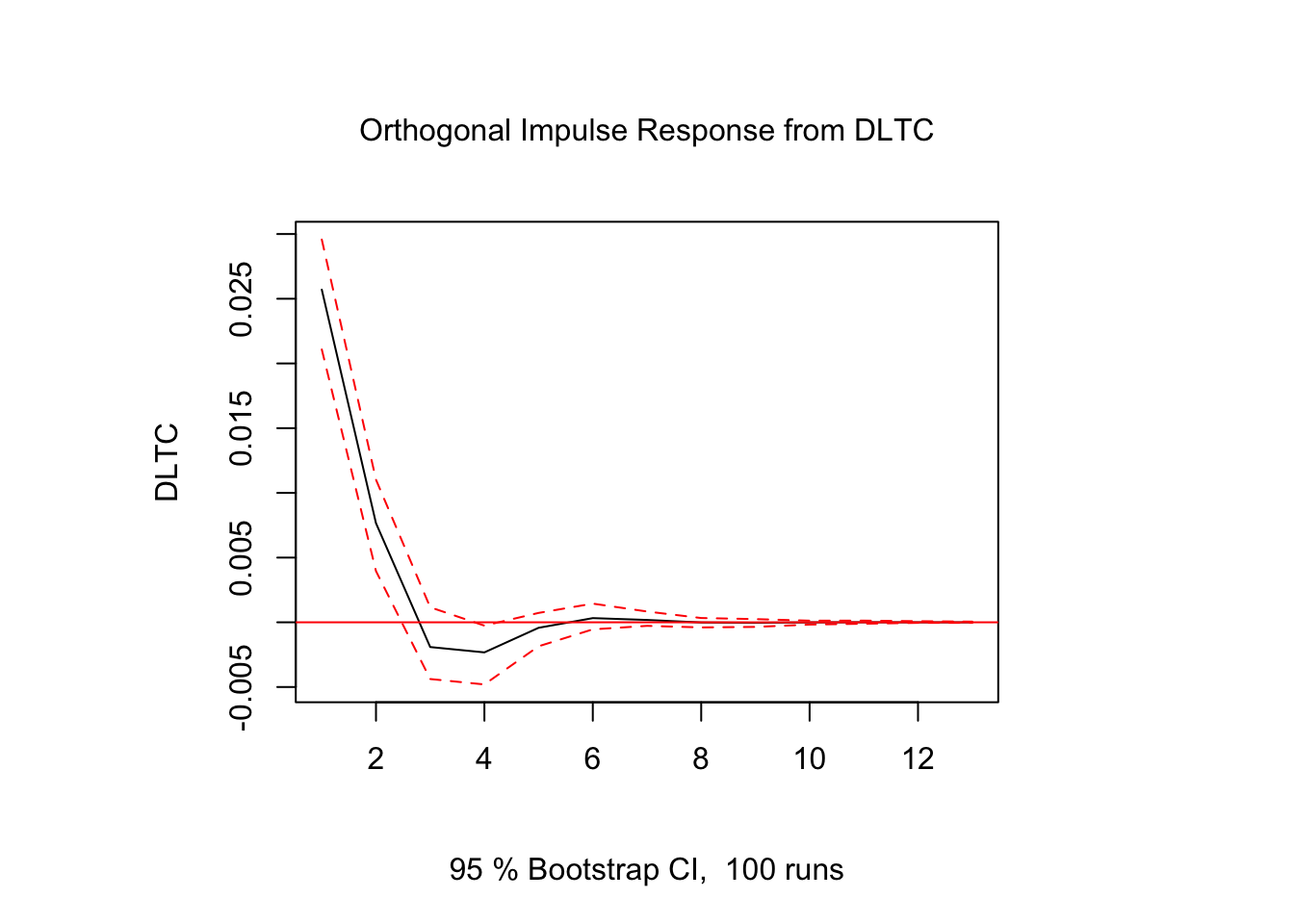

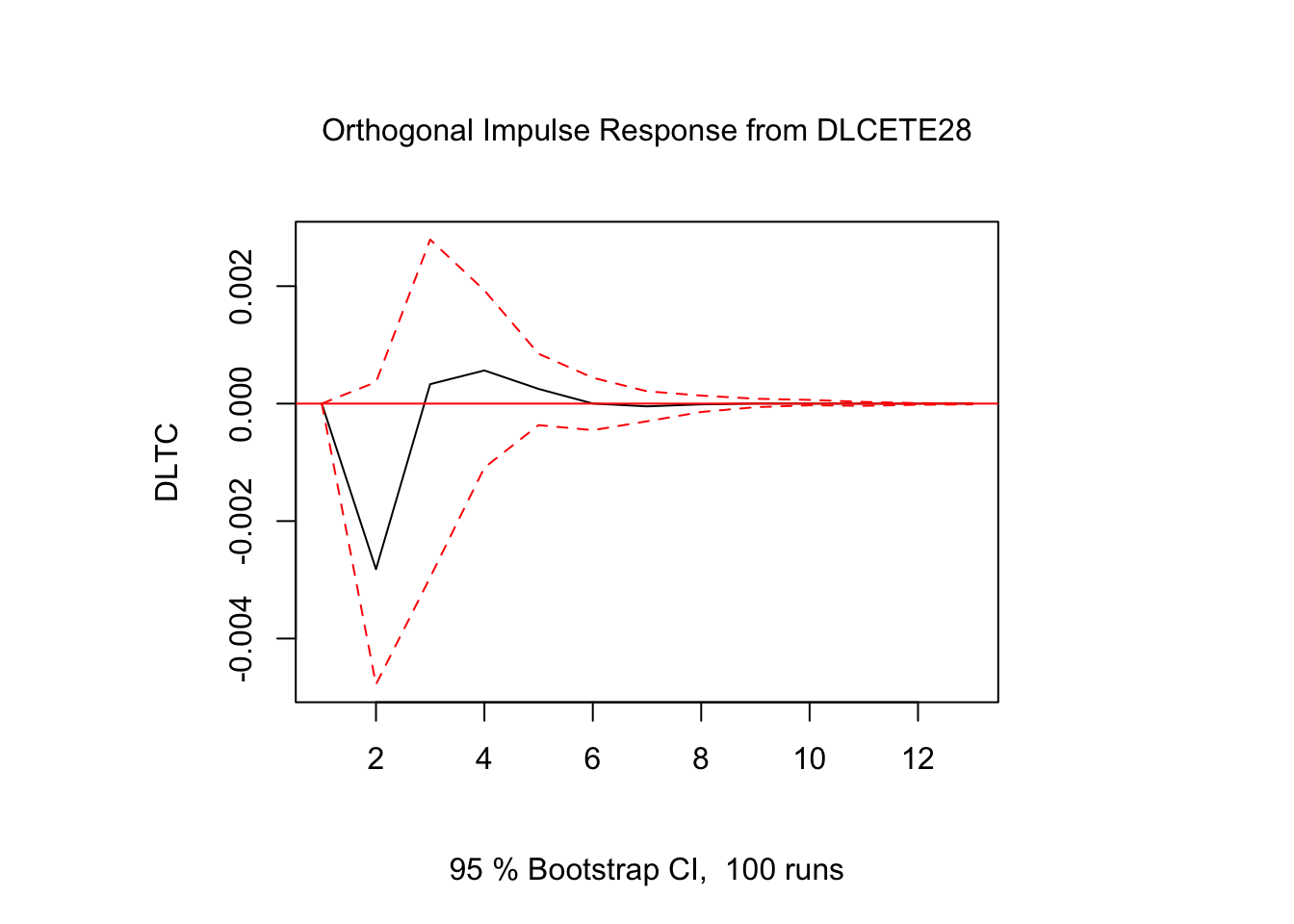

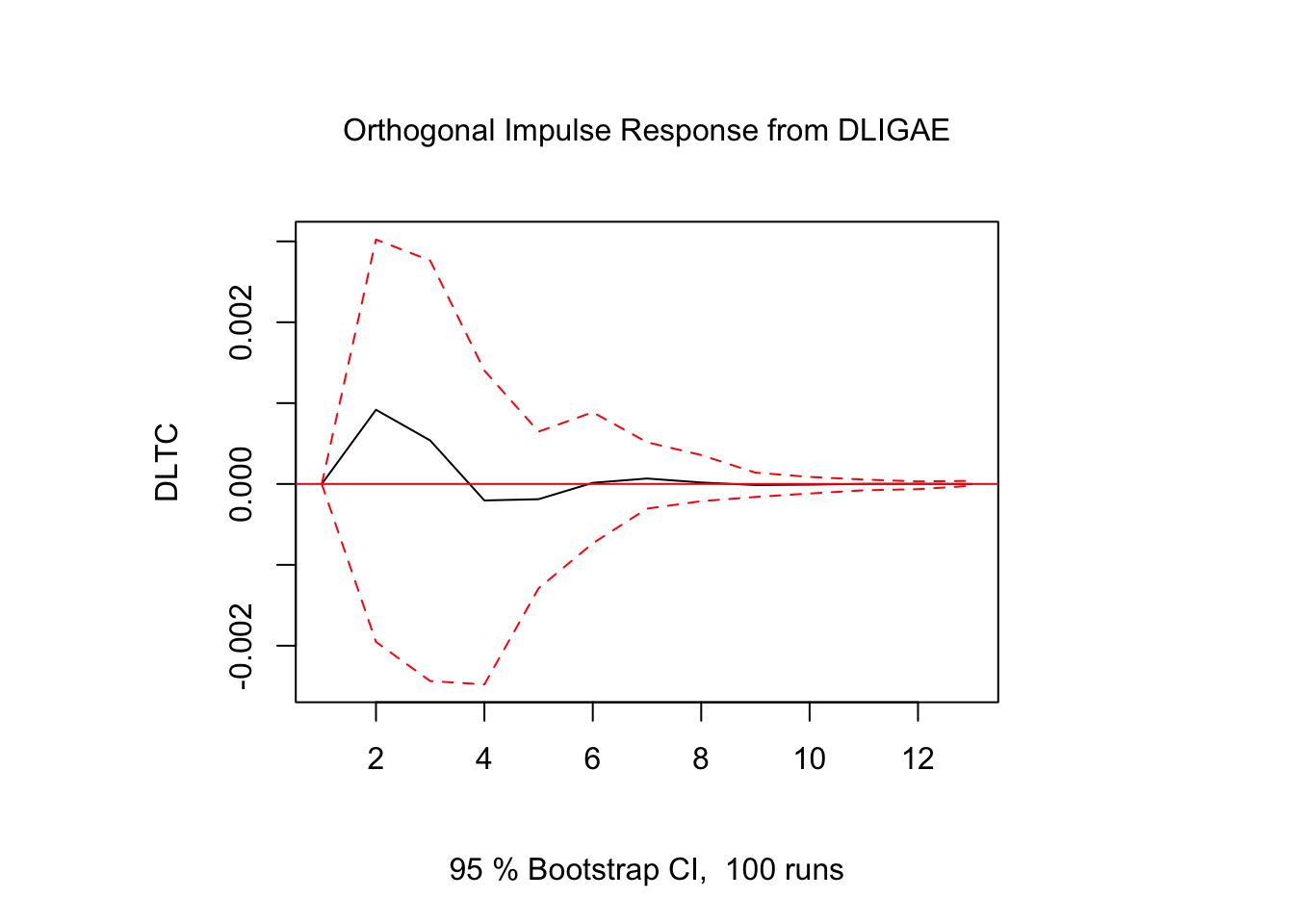

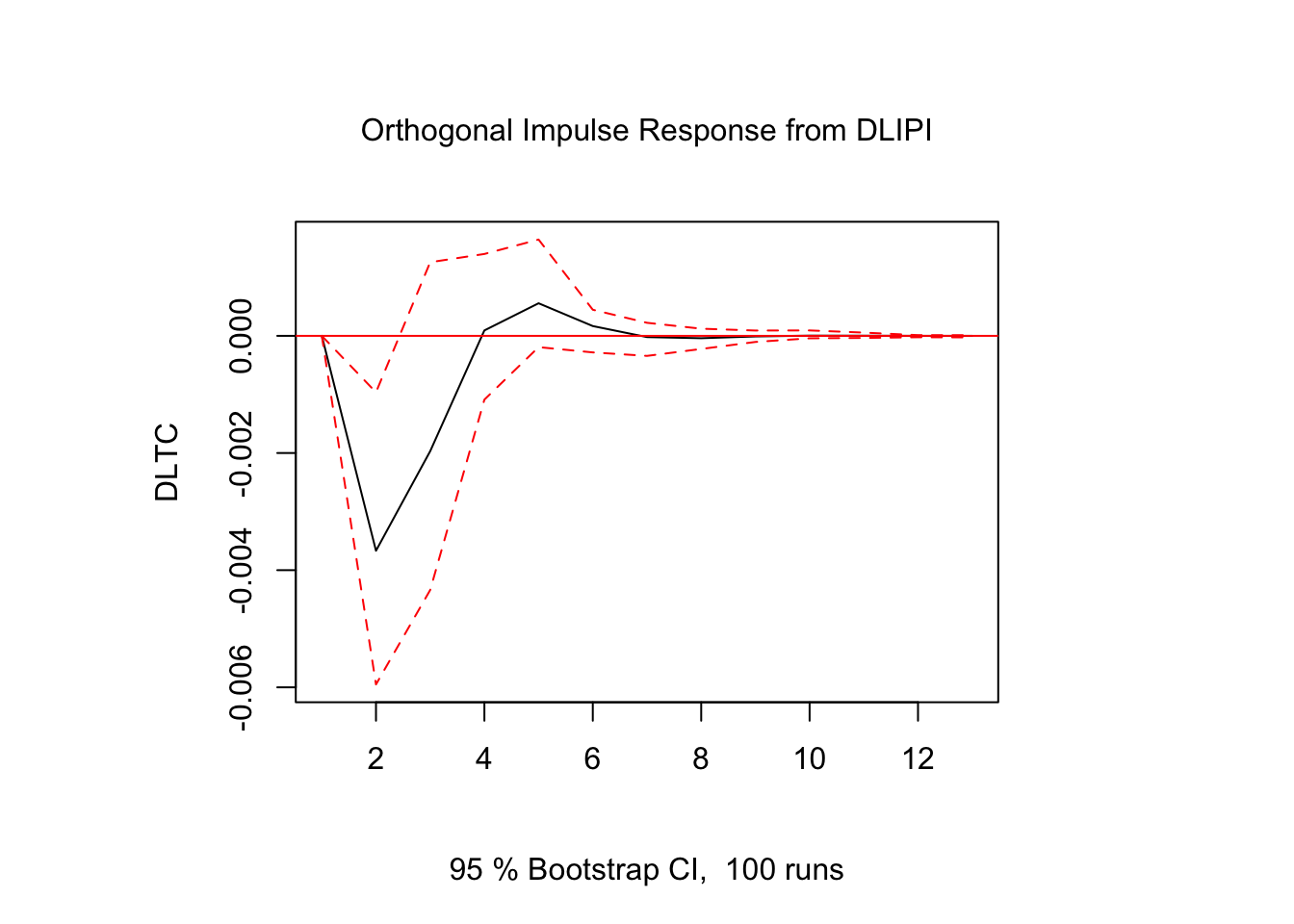

Figure 5.4: Impulso - Respuesta en \(DLTC_t\)

Figure 5.5: Impulso - Respuesta en \(DLTC_t\)

Figure 5.6: Impulso - Respuesta en \(DLTC_t\)

Figure 5.7: Impulso - Respuesta en \(DLTC_t\)

Figure 5.8: Impulso - Respuesta en \(DLTC_t\)

Los resultados muestran que la respuesta de \(DLTC_t\) ante impulsos en los términos de error fue estadísticamente significativo sólo para alguunos de los casos y en periodos cortos de tiempo. El resto de los resultados de Impulso-Respuesta se encuentra en el Scrip llamado Clase 15 que se ubica en el repositorio de GitHub.

5.4 Identificación de los Choques Estructurales en los Modelos VAR

En su trabajo seminal “Macroeconomics and Reality”, Sims (1980) cuestionó los modelos macroeconométricos utilizados en ese momento. Antes de la aparición de los modelos de referencia modernos, como los Vectores Autorregresivos (VAR) y los modelos estocásticos dinámicos de equilibrio general (DSGE), se estimaban modelos de ecuaciones simultáneas derivados de la escuela keynesiana, especificados con \(n\) cantidad de ecuaciones. Por lo tanto, para entender el surgimiento de los modelos VAR en la macroeconometría, es necesario partir del contexto en el que se escribió el trabajo seminal de Sims.

A finales de los años 70 e inicios de los 80, comenzó una crisis en torno a los modelos estructurales tradicionales. Los modelos macroeconómicos de gran escala –como los de la Cowles Commission– utilizaban restricciones teóricas para identificar relaciones estructurales que, en muchos casos, eran impuestas de manera arbitraria. Estos modelos estaban altamente parametrizados y basados en supuestos teóricos fuertes –como las expectativas adaptativas–, lo que los hacía sensibles a errores específicos. De esta situación surge en parte la Crítica de Lucas, en la cual Robert Lucas (1976) mostró que este tipo de modelos fallaba al capturar cambios en el comportamiento cuando las políticas cambiaban, debido a que no trataban adecuadamente las expectativas racionales.

Ante este panorama, Sims propuso los modelos VAR, lo que eventualmente le valió el Premio Nobel de Economía. El objetivo de estos modelos era ofrecer una alternativa más flexible y empíricamente realista, sin imponer supuestos estructurales fuertes a priori. De esta manera, los VAR permiten modelar un conjunto de variables macroeconómicas como funciones de sus propios rezagos, sin imponer una estructura teórica rígida. Además, todos los choques y relaciones se tratan inicialmente de forma simétrica y empírica. Así, los modelos VAR en su forma reducida son modelos completamente ateóricos.

Sin embargo, aunque los modelos VAR permiten capturar la dinámica conjunta entre variables sin imponer restricciones teóricas fuertes a priori, tienen una limitación que no es menor: los choques estimados a partir de la forma reducida -forma que hemos trabajado hasta ahora- están correlacionados entre sí. Es decir, los errores \(u_t\) de la forma reducida reflejan combinaciones lineales de múltiples choques estructurales y esto nos impide identificar la interacción contemporánea de las variables. Los choques \(u_t\) no se pueden interpretar directamente porque no son ortogonales. En este sentido, para encontrar choques estructurales, debemos encontrar choques \(w_t\) que sí sean ortogonales y tengan una interpretación económica.

Comencemos con la forma estructural del VAR para comprender sus parámetros: \[\begin{equation} B_0 Y_t = B_1 Y_{t-1} + ... B_p Y_{t-p} + w_t \end{equation}\]

donde \(w_t\) es un término de error con media cero y no correlacionado en el tiempo, también conocido como innovación estructural o shock estructural. Además, se asume que el término de error es incondicionalmente homocedástico a menos de que se indique lo contrario. La matriz \(B_0\) es no singular y establece la interacción contemporánea entre las variables del modelo. De este modo, el modelo puede escribirse de manera compacta como: \[\begin{equation} B(L) y_t = w_t \end{equation}\]

donde \(B(L) \equiv B_0 - B_1 L - B_2 L^2 - ...B_p L^p\) es el polinomio autorregresivo en rezagos. La matriz de covarianza del término de error estructural es normalizada tal que: \[\begin{equation} \mathbb{E}(w_t w_t') \equiv \Sigma_w = I_K. \end{equation}\]

Con esto, sabemos que existen tantos shocks estructurales como variables en el modelo. Asimismo, los shocks estructurales, por definición, son mutuamente no correlacionados lo que implica que \(\Sigma_w\) es diagonal. Por último, también sabemos que si normalizamos la varianza de todos los shocks estructurales a uno, no implica una pérdida de generalidad siempre y cuando los elementos diagonales \(B_0\) permanezcan sin restricciones.

Sin embargo, para que el modelo \(B_0 Y_t = B_1 Y_{t-1} + ... B_p Y_{t-p} + w_t\) sea considerado como un VAR estructural no es suficiente con que los elementos de \(w_t\) no se encuentren correlacionados, si no que los choques también deben ser económicamente interpretables. Para esto, derivamos la forma reducida de este modelo VAR estructural de tal modo que \(y_t\) es una función de los rezagos de \(y_t\) únicamente. Si multiplicamos ambos lados de la representación estructural del VAR por \(B_0^{-1}\) \[\begin{equation} B_0^{-1} B_0 y_t = B_0^{-1} B_1 y_{t-1} + ... + B_0^{-1} B_p y_{t-p} + B_0^{-1} w_t \end{equation}\]

de tal modo que puede ser representado como \[\begin{equation} y_t = A_1 y_{t-1} + ... + A_p y_{t-p} + u_t \end{equation}\]

donde \(A_i = B_0^{-1} B_i\), \(i = 1,...,p\), y \(u_t = B_0^{-1} w_t\). Asi, las innovaciones en forma reducida de \(u_t\) son un promedio ponderado de los shocks estructurales \(w_t\). De manera compacta, el modelo puede ser expresado como: \[\begin{equation} A(L) y_t = u_t \end{equation}\]

donde \(A(L) = I_K - A_1L - A_2 L^2 - ... A_p L^p\) es el polinomio autorregresivo en rezagos. Los métodos de estimación estándar permiten obtener estimaciones de los parámetros de la forma reducida \(A_i\), para \(i=1,...p\), de las innovaciones reducidas \(u_t\) y de su matriz de covarianza \(\mathbb{E}(u_t u_t') \equiv \Sigma_u\).

Sin embargo, el debate que se ha generado desde entonces es, una vez estimada la forma reducida, de qué manera se puede recuperar la representación estructural del modelo VAR. Es decir, queremos recuperar la matriz \(B_0\) -o bien, su inversa- que contiene las relaciones estructurales contemporáneas de las variables, recordando que \(u_t = B_0^{-1}w_t\).

El método para recuperar dicha matriz ha generado gran debate en el análisis macroeconométrico, dando pie incluso a tesis doctorales al respecto. Con esto en mente, ahora veremos algunos de los métodos clásicos para recuperar las relaciones estructurales de las variables. Nos concentraremos en los siguientes:

1. Identificación Recursiva

2. Restricción de largo plazo

3. Imposición de restricciones de signo

Nota: RStudio es un poco limitado en cuanto a los métodos de identificación de las innovaciones estructurales relacionados con la teoría económica. En realidad, en los trabajos actuales de macroeconometría suele ocuparse, mayoritariamente, el método de Identificación Recursiva. Sin embargo, para ver los métodos de Restricción de largo plazo e Imposición de restricciones de signo, ver el Script de MatLab de estos.

5.4.1 VAR Recursivo - Identificación Recursiva

Una de las formas más populares para recuperar las innovaciones estructurales es mediante la identificación recursiva, un caso particular de las restricciones de corto plazo que se implementa utilizando la descomposición de Cholesky.

La idea detrás de este método es simple e intuitivo: queremos recuperar las innovaciones estructurales \(w_t\) a partir de las innovaciones de forma reducida \(u_t\). Para lograr esto, buscamos ortogonalizar los errores de forma reducida, lo que en este contexto significa transformarlos en un conjunto de choques no correlacionados contemporáneamente. Es decir, deseamos que \(\mathbb{E}[w_t w_t'] = I\).

Para lograr esto, definimos una matriz \(P\) de tamaño \(K \times K\), triangular inferior y con diagonal principal positiva, de tal modo que:

\[\begin{equation} \Sigma_u = \mathbb{E}[u_t u_t'] = P P' \end{equation}\]

La matriz \(P\) es conocida como la descomposción de Cholesky inferior de \(\Sigma_u\). Por ejemplo, en un VAR con tres variables, \(P\) tendría la forma:

\[ P = \begin{bmatrix} p_{11} & 0 & 0 \\ p_{21} & p_{22} & 0 \\ p_{31} & p_{32} & p_{33} \end{bmatrix} \]

Ahora, si recordamos que en el modelo estructural los errores están relacionados por \(u_t = B_0^{-1}w_t\) y que

\[\begin{equation} \Sigma_u = B_0^{-1} \mathbb{E}[w_t w_t'] B_0^{-1'} = B_0^{-1} B_0^{-1'} \end{equation}\]

entonces una solución válida al problema de identificación estructural es asumir que \(B_0^{-1} = P\). Dado que \(P\) es triangular inferior, contiene exactamente \(\frac{K(K-1)}{2}\) ceros impuestos, lo que cumple la condición de orden para identificar todos los elementos libres de la matriz \(B_0^{-1}\). Por simetría. si \(B_0^{-1}\) es triangular inferior, entonces \(B_0\) también lo es -aunque triangular superior-.

Sin embargo, es importante destacar que esta ortogonalización de los errores solo es válida si la estructura recursiva impuesta por la matriz \(P\) se puede justificar con fundamentos económicos. El método impone que la primera variable del sistema responde solo a su propio shock contemporáneo, la segunda puede responder al shock de la primera, la tercera a los dos primeros, y así sucesivamente. Por eso se dice que el modelo estructural resultante es recursivo: se impone una estructura jerárquica de causalidad contemporánea, en lugar de inferirla directamente de los datos.

En este sentido, la descomposición de Cholesky no descubre las relaciones estructurales sino que las impone. Por lo tanto, el orden de las variables en el VAR si importa, ya que determina la interpretación de los shocks estructurales. Por esta razón, se recomienda justificar el orden mediante teoría económica. Por ejemplo, en aplicaciones del Banco de México, el orden se suele establecer de acuerdo con la hipótesis de una economía pequeña y abierta, ordenando las variables de la más exógena a la más endógena.

Veamos un ejemplo rápido de la identificación recursiva mediante la descomposición de Cholesky:

# install.packages("svars")

# install.packages("ggplot2")

# install.packages("ggfortify")

library(svars)

library(ggplot2)

library(ggfortify)

var.reducido <- vars::VAR(USA, lag.max = 10, ic = "AIC")

var.estructural <- id.chol(var.reducido)

summary(var.estructural)##

## Identification Results

## ----------------------

##

## Method: Cholesky

## Sample size: 169

##

## Estimated B Matrix (unique decomposition of the covariance matrix):

## [,1] [,2] [,3]

## x 0.68338360 0.0000000 0.0000000

## pi -0.03642697 1.0726563 0.0000000

## i 0.22450359 0.1818031 0.7672318# x = Porcentaje de desviación logarítmica del PIB real con respecto a la

# estimación del producto potencial

# pi = Crecimiento anualizado trimestre a trimestre del deflactor del PIB

# i = Tasa de interés de los fondos federales

cores <- parallel::detectCores() - 1

boot.svar <- wild.boot(var.estructural, n.ahead = 24, nboot = 1000, nc = cores)

plot(boot.svar)

5.4.2 VAR Estructural - Restricción de largo plazo

Otra manera de identificar las innovaciones estructurales de un modelo VAR, es mediante el método propuesto por Blanchard y Quah (1989) en “The Dynamic Effects of Aggregate Demand and Supply Disturbances”.

La intuición de este método es simple: Blanchard y Quah querían medir el efecto de choques de oferta agregada \(w_t^{AS}\) y demanda agregada \(w_t^{AD}\) sobre el Producto y el Desempleo, imponiendo restricciones en la respuesta acumulada, es decir, en el efecto acumulado permanente (horizonte \(h \rightarrow \infty\)). La lógica económica detrás de este método es, básicamente, que el choque de demanda agregada no tiene efectos de largo plazo sobre el nivel del PIB real.

Ahora bien, sean:

- \(ur_t\): tasa de desempleo en EE.UU.

- \(gdp_t\): logaritmo del PIB real de EE.UU.

Y definimos el vector \(z_t\)

\[\begin{equation} z_t = \begin{bmatrix} \Delta gdp_t \\ ur_t \end{bmatrix} \sim I(0) \end{equation}\]

Aunque \(gdp_t \sim I(1)\), su primera diferencia es estacionaria (\(I(0)\)), lo cual justifica que \(z_t \sim I(0)\). Por otro lado, podemos suponer que este vector es generado por un VAR reducido:

\[\begin{equation} A(L) z_t = u_t \end{equation}\]

donde \(A(L)=I_2-A_1L-...A_pL^p\), y \(u_t \sim (0, \Sigma_u)\) es ruido blanco. Si lo representamos como su forma estructural, tenemos que:

\[\begin{equation} B(L) z_t = w_t \end{equation}\]

donde \(B(L) = B_0-B_1L-...B_pL^p = B_0A(L)\), y si recordamos a qué es igual \(w_t\), tenemos que:

\[\begin{equation} w_t = B_0 u_t \rightarrow u_t = B_0^{-1} w_t \rightarrow \Sigma_u = B_0^{-1} (B_0^{-1})' \end{equation}\]

Ahora, pasemos a la representación MA estructural para entender dónde se impone la restricción. Desde el modelo MA, tenemos que:

\[\begin{equation} z_t = B(L)^{-1} w_t = \Theta (L) w_t \end{equation}\]

Esto implica que, dado que \(z_t \sim I(0)\), el efecto de un choque estructural sobre \(z_t\) se desvanece con el tiempo y, por tanto, tanto \(\Delta gdp_t\) como \(ur_t\) eventualmente vuelven a su nivel original tras un choque. Sin embargo, el nivel del PIB real -y no su crecimiento- no necesariamente vuelve a su nivel inicial, por lo que la suma acumulada de las respuestas al choque nos da su efecto permanente. Ahora, pasemos a la matriz de efectos acumulados de largo plazo, definida como:

\[\begin{equation} \Theta (1) = \sum_{i=0}^{\infty} \Theta_i = B(1)^{-1} \end{equation}\]

Dado que queremos que el PIB real vuelva a su tendencia tras un choque de demanda -recordemos que no tiene efectos de largo plazo- implica imponer un cero en la posición \(\theta_{12}\) de la matriz \(\Theta(1)\):

\[\begin{equation} \Theta (1) = \begin{bmatrix} \theta_{11} (1) & 0 \\ \theta_{21} (1) & \theta_{22} (1) \end{bmatrix} \end{equation}\]

el hecho de que \(\theta_{12}(1) = 0\) implica que el choque de demanda no afecta permanentemente al PIB real y, por otro lado, que \(\theta_{11}(1)\) permanezca libre, implica que los choques de oferta sí pueden tener efectos de largo plazo.

Para la identificación, recordemos que:

\[\begin{equation} \Theta (1) = B(1)^{-1} = A(1)^{-1} B_0^{-1} \rightarrow B_0^{-1} = A(1) \Theta(1) \end{equation}\]

De este modo, una vez que conocemos \(A(1)\) y \(\Theta(1)\) podemos recuperar \(B_0^{-1}\), recordando que la restricción en \(\Theta(1)\) es equivalente a imponer una restricción sobre \(B_0\).

Para estimar \(\Theta(1)\), sabemos que:

\[\begin{equation} \Sigma_u = B_0^{-1} (B_0^{-1})' = \Theta(1) \Theta(1)' \end{equation}\]

y, entonces, si usamos \(A(1)\):

\[\begin{equation} A(1)^{-1} \Sigma_u A(1)^{-1'} = \Theta(1) \Theta(1)' \end{equation}\]

lo cual implica que podemos calcular el lado izquierdo usando solo parámetros estimados del VAR reducido y luego identificar \(\Theta(1)\) imponiendo que tenga forma triangular inferior, y aplicar la descomposición de Cholesky para tener finalmente que:

\[\begin{equation} B_0^{-1} = A(1) \Theta (1) \end{equation}\]

5.4.3 VAR Estructural - Imposición de restricciones de signo

Una alternativa a la identificación de las innovaciones estructurales además de la Identificación recursiva es la Imposición de restricciones de signo. Sigue un poco la misma lógica: queremos imponer restricciones de signo en vez de proponer una matriz triangular inferior en la matriz \(B_0^{-1}\). Este método ofrece una alternativa menos restrictiva que imponer ceros exactos. Para explicar este método, tomemos el siguiente modelo ejemplo.

Consideremos un modelo bivariado de un mercado de bienes con:

- Un choque de demanda \(w_t^{demanda}\)

- Un choque de oferta \(w_t^{oferta}\)

en donde nuestras variables observables son:

- Precio \(p_t\)

- Cantidad \(q_t\)

Y los errores en forma reducida están dados por:

\[\begin{equation} u_t = \begin{bmatrix} u_t^q \\ u_t^p \end{bmatrix} = B_0^{-1} w_t \quad \text{donde} \quad w_t = \begin{bmatrix} w_t^{oferta} \\ w_t^{demanda} \end{bmatrix} \end{equation}\]

Es sencillo: la interpretación económica es que los efectos de los choques \(u_t\) dependen de la pendiente de las curvas de demanda y oferta.

En un método tradicional -restricción de exclusión-, se asume que la oferta es vertical en el corto plazo, lo cual implica que los choques de demanda no afectan la cantidad contemporáneamente:

\[\begin{equation} \begin{bmatrix} u_t^q \\ u_t^p \end{bmatrix} = \begin{bmatrix} \ast & 0 \\ \ast & \ast \end{bmatrix} \begin{bmatrix} w_t^{oferta} \\ w_t^{demanda} \end{bmatrix} \end{equation}\]

En donde los asteriscos representan coeficientes libres y el cero es una restricción de exclusión.

En cambio, si tomamos la teoría económica básica en el enfoque alternativo de Imposición de restricción de signo esperaríamos que, ante un choque de oferta positivo -la curva de oferta se desplaza a la derecha-, la cantidad aumente y el precio caiga, mientras que, ante un choque de demanda positiva -la curva de demanda se desplaza a la derecha-, la cantidad aumenta y el precio aumenta. De este modo, tenemos que:

\[\begin{equation} \begin{bmatrix} u_t^q \\ u_t^p \end{bmatrix} = \underbrace{ \begin{bmatrix} + & + \\ - & + \end{bmatrix} }_{B_0^{-1}} \begin{bmatrix} w_t^{\text{oferta}} \\ w_t^{\text{demanda}} \end{bmatrix} \end{equation}\]

Donde \(+\) indica signo positivo estricto y \(-\) negativo estricto.

La diferencia clave con el método de Identificación recursiva mediante la descomposición de Cholesky es que, en estos últimos modelos, los parámetros están puntualmente identificados mientras que con restricciones de signo los parámetros no se identifican exactamente, sino que quedan dentro de un conjunto compatible con las restricciones. De este modo, no hay una única solución, pues hay muchas matrices \(B_0^{-1}\) que cumplen con los signos impuestos. También, se pueden imponer restricciones de signo de la siguiente forma:

\[\begin{equation} \begin{bmatrix} + & + \\ 0 & + \end{bmatrix} \quad \text{o} \quad \begin{bmatrix} + & + \\ - & 0 \end{bmatrix} \end{equation}\]

Estas formas también pueden ser admisibles pero algunas podrían llegar a ser problemáticas si llevan a choques no identificables entre sí.

Se dice que los modelos identificados por signos son más generales que los recursivos pero no son modelos “anidados”, o sea, uno no puede validar o rechazar el otro con datos. Así, las restricciones de signo permiten más flexibilidad, pero imponen otras limitaciones como perder identificación puntual.

Ahora, de manera más puntual, para imponer las restricciones de signo estáticas consideremos un modelo VAR en su forma estructural:

\[\begin{equation} B_0 y_t = B_1 y_{t-1} + ... + B_p y_{t-p} + w_t \end{equation}\]

y normalizamos la matriz de varianzas-covarianzas del término de error estructural \(w_t\) tal que:

\[\begin{equation} \mathbb{E}(w_t w_t') \equiv \Sigma_w = I_K. \end{equation}\]

Ahora, sea \(u_t = P \eta_t\), donde \(u_t\) es la innovación del VAR en forma reducida y \(P\) es la descomposición de Cholesky de \(\Sigma_u\). Por construcción, los choques \(\eta_t\) son mutuamente no correlacionados y tienen varianza unitaria. Por supuesto, no hay razón para que estos choques correspondan a choques estructurales económicamente interpretables, como los choques de oferta y demanda en el modelo bivariado mencionado anteriormente. Sin embargo, podemos buscar soluciones candidatas \(w_t^*\) para los choques estructurales desconocidos \(w_t\) construyendo un gran número de combinaciones de los choques \(\eta_t\) de la forma:

\[\begin{equation} w_t^* = Q' \eta_t, \end{equation}\]

donde \(Q'\) es una matriz ortogonal cuadrada tal que \(Q'Q = QQ' = I_K\) y \(u_t = PQ \eta_t = PQw_t^*\). Por lo tanto, cada solución candidata \(w_t^*\) consiste en choques no correlacionados con varianza unitaria. Que una de estas soluciones candidatas \(w_t^*\) sea una solución admisible para el choque estructural desconocido \(w_t\), dado el vector de parámetros en forma reducida, depende de si la matriz de impacto estructural implicado \(PQ\) satisface las restricciones de signo mantenidas sobre \(B_0^{-1}\). De este modo, solo conservamos las soluciones que satisfagan las restricciones de signo y se descartan las demás. El hecho de repetir este procedimiento nos permite caracterizar el conjunto de todos los modelos estructurales que son consistentes con las restricciones de signo mantenidas y los parámetros en forma reducida. Conocer \(PQ\) permite construir todos los coeficientes estructurales de respuesta al impulso que se derivan de las estimaciones de los parámetros en forma reducida.

Los dos enfoques comunes para construir las matrices ortogonales \(Q\) están basados en:

Matrices de rotación de Givens.

Transformación de Householder.

La paquetería del código de MatLab, VAR Toolbox, ocupa el enfoque de Matrices de rotación de Givens.

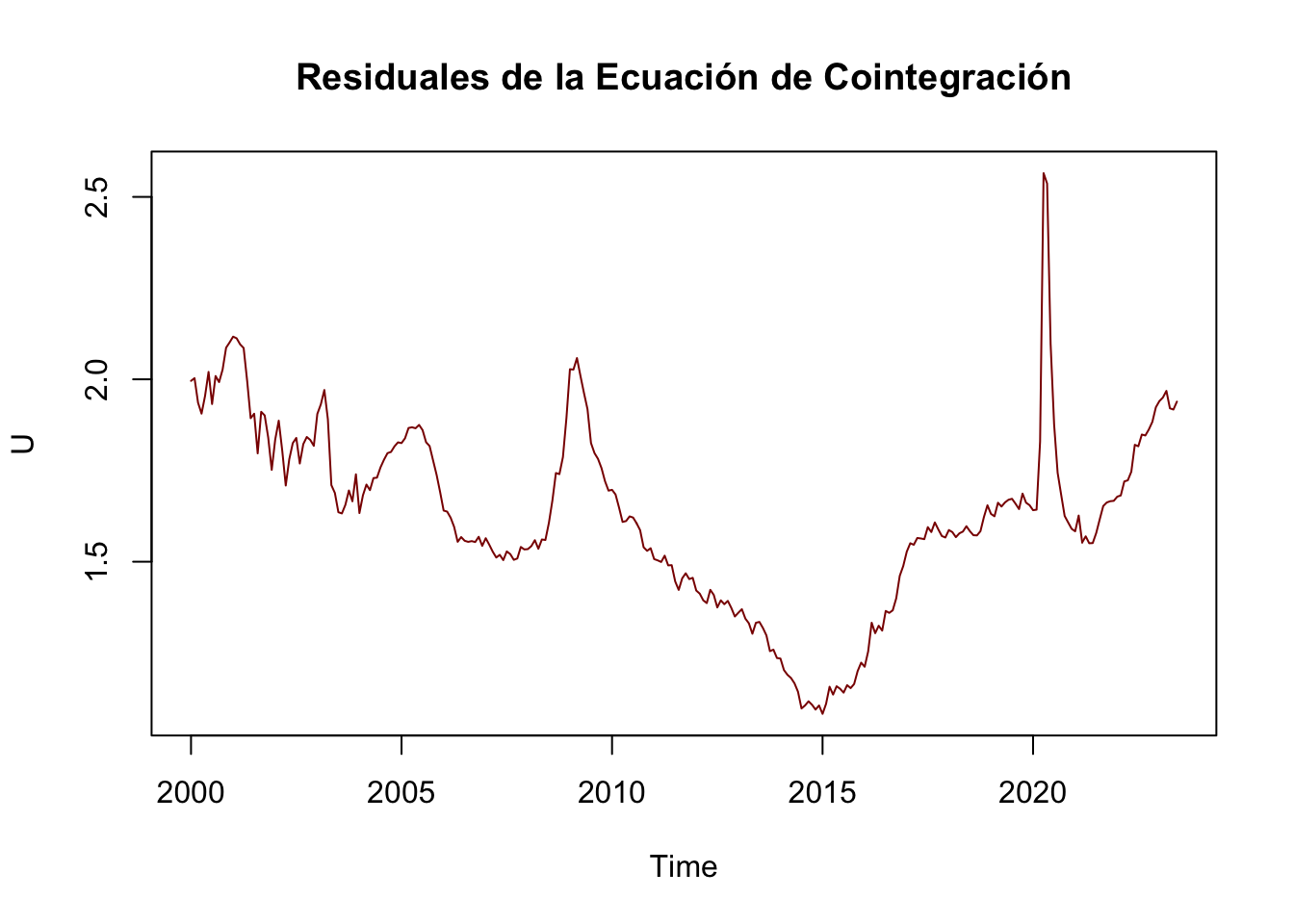

5.5 Cointegración

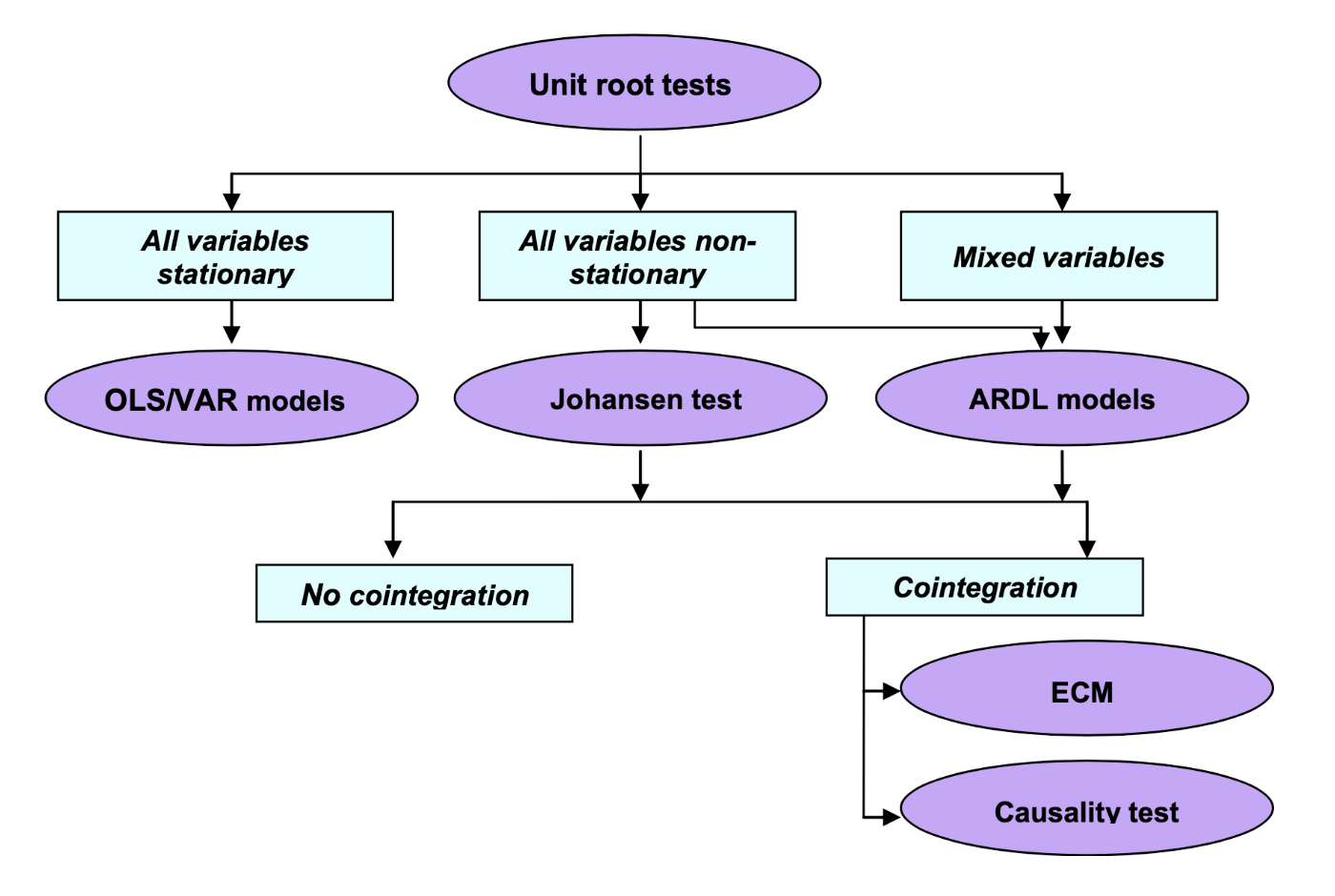

Hasta ahora en el curso hemos usado el supuesto de que las series son estacionarias para el conjunto de técnicas \(ARMA(p,q)\) y \(VAR(p)\). No obstante, dado que relajamos el supuesto de estacionariedad (incluyendo la estacionariedad en varianza) y que establecimos una serie de pruebas para determinar cuándo una serie es estadísticamente estacionaria, ahora podemos plantear una técnica llamada Cointegración. Para esta técnica consideraremos sólo series que son \(I(1)\) y reconoceremos que se originó con los trabajos de Engle y Granger (1987), Stock (1987) y Johansen (1988).

5.5.1 Definición y propiedades del proceso de cointegración

Cointegración puede ser caracterizada o definida en palabras sencillas como que dos o más variables tienen una relación común estable en el largo plazo. Es decir, estas no suelen tomar caminos o trayectorias diferentes, excepto por períodos de tiempo transitorios y eventuales. A continuación, utilizaremos la definición de Engle y Granger (1984) de cointegración.

Sea \(\mathbf{Y}\) un vector de k-series de tiempo, decimos que los elementos en \(\mathbf{Y}\) están cointegrados en un orden (d, c), es decir, \(\mathbf{Y} \sim CI(d, c)\), si todos los elementos de \(\mathbf{Y}\) son series integradas de orden d, I(d), y si existe al menos una combinación lineal no trivial \(\mathbf{Z}\) de esas variables que es de orden I(d - c), donde \(d \geq c > 0\), si y sólo si: \[\begin{equation} \boldsymbol{\beta}_i' \mathbf{Y}_t = \mathbf{Y}_{it} \sim I(d-c) \end{equation}\]

Donde \(i = 1, 2, \ldots, r\) y \(r < k\).

A los diferentes vectores \(\boldsymbol{\beta}_i\) se les denomina como vectores de cointegración. El rango de la matriz de vectores de cointegración \(r\) es el número de vectores de cointegración linealmente independientes. En general diremos que los vectores de la matriz de cointegración \(\boldsymbol{\beta}\) tendrán la forma de: \[\begin{equation} \boldsymbol{\beta}' \mathbf{Y}_t = \mathbf{Z}_t \end{equation}\]

Antes de continuar hagamos algunas observaciones. Si todas las variables de \(\mathbf{Y}\) son I(1) y \(0 \leq r < k\), diremos que las series no cointegran si \(r = 0\). Si esto pasa, entonces, como demostraremos más adelante, la mejor opción será estimar un modelo VAR(p) en diferencias. Adicionalmente, asumiremos que \(c = d = 1\), por lo que la relación de cointegración, en su caso, generará combinaciones lineales \(\mathbf{Z}\) estacionarias.

5.5.2 Cointegración para modelos de más de una ecuación o para modelos basados en Vectores Autoregresivos

Sean \(Y_1, Y_2, \ldots, Y_k\) son series que forman \(\mathbf{Y}\) y que todas son I(1), entonces los siguientes casos son posibles:

Si \(r = 1\) entonces se trata de un caso de cointegración de Granger.

Si \(r \geq 1\) entonces se trata de un caso de cointegración múltiple de Johansen.

Por lo anterior, en este curso analizaremos el caso de Cointegración de Johansen. Ahora plantearemos la forma de estimar el proceso de cointegración. El primer paso para ello es determinar un modelo VAR(p) con las k-series no estacionarias (series en niveles)–en este punto se vuelve fundamental caracterizar las series a través de pruebas de raíces unitarias–. Elegimos el valor de \(p\) mediante el uso de los criterios de información. De esta forma tendremos una especificación similar a: \[\begin{equation} \mathbf{Y}_t = \sum_{j=1}^p \mathbf{A}_j \mathbf{Y}_{t-j} + \mathbf{D}_t + \mathbf{U}_t \tag{5.2} \end{equation}\]

Donde \(\mathbf{U}_t\) es un término de error k-dimensional puramente aleatorio; \(\mathbf{D}_t\) contiene los componentes determinísticos de constante y tendencia, y \(\mathbf{A}_i\), \(i = 1, 2, \ldots, p\), son matrices de \(k \times k\) coeficientes. Notemos que el VAR(p) involucrado en este caso, a diferencia del VAR anteriormente estudiado, puede incluir un término de tendencia. Esto en razón de que hemos relajado el concepto de estacionariedad.

Si reescribimos la ecuación (5.2) en su forma de Vector Corrector de Errores (VEC, por sus siglas en inglés) tenemos: \[\begin{eqnarray} \mathbf{Y}_t - \mathbf{Y}_{t-1} & = & \Delta \mathbf{Y}_t \nonumber \\ & = & \sum_{j=1}^p \mathbf{A}_j \mathbf{Y}_{t-j} + \mathbf{D}_t - \mathbf{Y}_{t-1} + \mathbf{U}_t \nonumber \\ & = & (\mathbf{A}_1 - \mathbf{I}) \mathbf{Y}_{t-1} + \mathbf{A}_2 \mathbf{Y}_{t-2} + \ldots + \mathbf{A}_p \mathbf{Y}_{t-p} + \mathbf{D}_t + \mathbf{U}_t \nonumber \\ & = & \left( \sum_{j=1}^{p} \mathbf{A}_j - \mathbf{I} \right) \mathbf{Y}_{t-1} + \sum_{j=1}^{p-1} \mathbf{A}^*_j \Delta \mathbf{Y}_{t-j} + \mathbf{D}_t \mathbf{U}_t \nonumber \\ & = & - \left( \mathbf{I} - \sum_{j=1}^{p} \mathbf{A}_j \right) \mathbf{Y}_{t-1} + \sum_{j=1}^{p-1} \mathbf{A}^*_j \Delta \mathbf{Y}_{t-j} + \mathbf{D}_t \mathbf{U}_t \nonumber \\ \Delta \mathbf{Y}_t & = & - \Pi \mathbf{Y}_{t-1} + \sum_{j=1}^{p-1} \mathbf{A}^*_j \Delta \mathbf{Y}_{t-j} + \mathbf{D}_t + \mathbf{U}_t \tag{5.3} \end{eqnarray}\]

Donde \(\mathbf{A}_j^* = - \sum_{i=j+1}^p \mathbf{A}_i\), \(i = 1, 2, \ldots, p-1\), y la matriz \(\Pi\) representa todas las relaciones de largo plazo entre las variables, por lo que la matriz es de rango completo \(k \times k\). Por lo tanto, tenemos que dicha matriz en la ecuación (5.3) se puede factorizar como: \[\begin{equation} \Pi_{(k \times k)} = \Gamma_{(k \times r)} \boldsymbol{\beta}_{(r \times k)}' (\#eq:Pi_Matrix) \end{equation}\]

Donde \(\boldsymbol{\beta}_{(r \times k)}' \mathbf{Y}_{t-1}\) son \(r\) combinaciones linealmente independientes que son estacionarias.

Dada la ecuación (5.3) podemos establecer la aproximación de Johansen (1988) que se realiza mediante una estimación por Máxima Verosimilitud de la ecuación: \[\begin{equation} \Delta \mathbf{Y}_t + \Gamma \boldsymbol{\beta}' \mathbf{Y}_{t-1} = \sum_{j=1}^{p-1} \mathbf{A}^*_j \Delta \mathbf{Y}_{t-j} + \mathbf{D}_t + \mathbf{U}_t \end{equation}\]

Donde una vez estimado el sistema: \[\begin{equation} \boldsymbol{\beta} = [v_1, v_2, \ldots, v_r] \end{equation}\]

Cada \(v_i\), \(i = 1, 2, \ldots, r\) es un vector propio que está asociado con los \(r\) valores propios positivos, mismos que están asociados con la prueba de hipótesis de cointegración. Dicha hipótesis está basada en dos estadísticas con las que se determina el rango \(r\) de \(\Pi\):

Prueba de Traza: \(H_0 :\) Existen al menos \(r\) valores propios positivos o Existen al menos \(r\) relaciones de largo plazo estacionarias.

Prueba del valor propio máximo o \(\lambda_{max}\): \(H_0 :\) Existen \(r\) valores propios positivos o Existen \(r\) relaciones de largo plazo estacionarias.

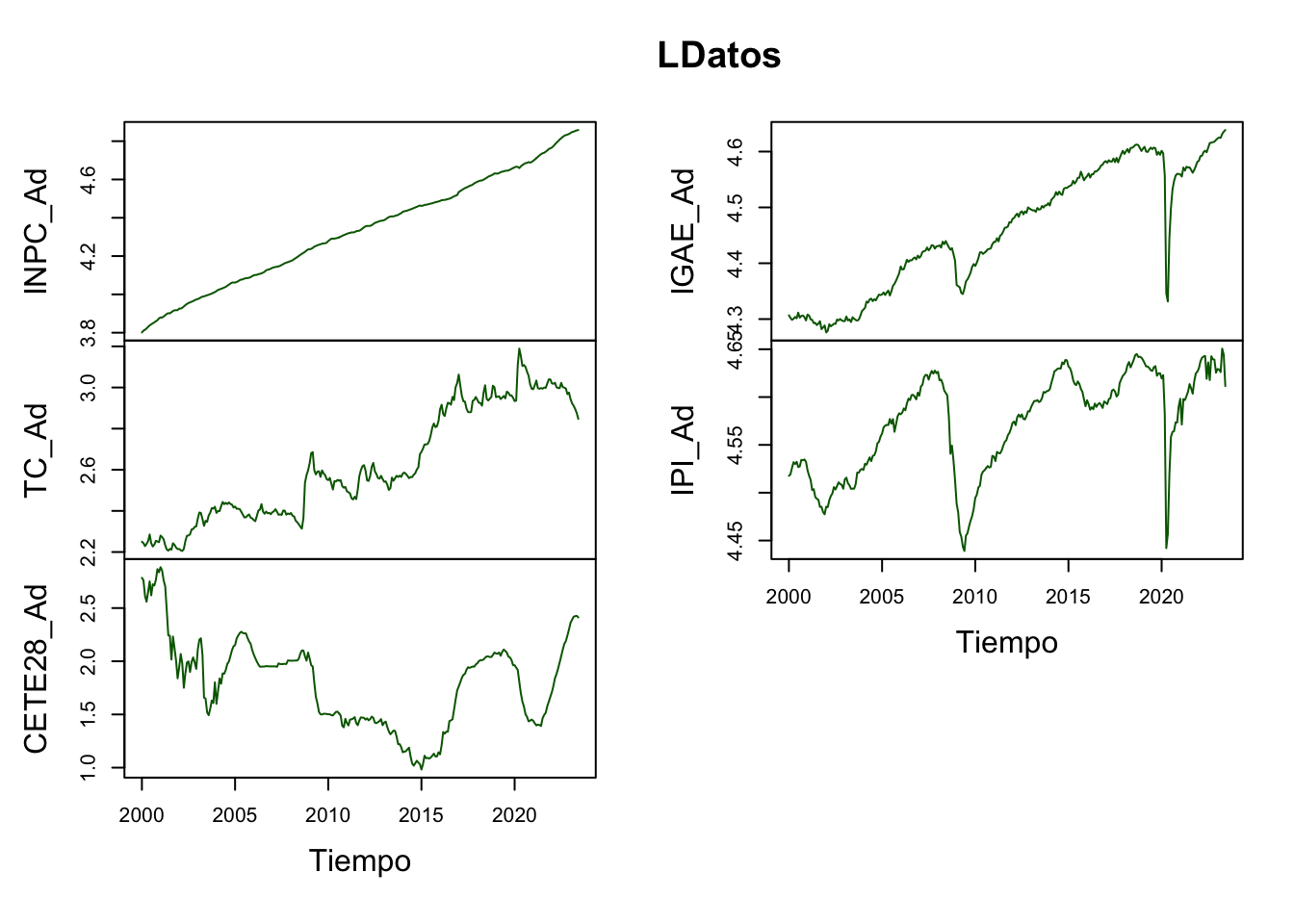

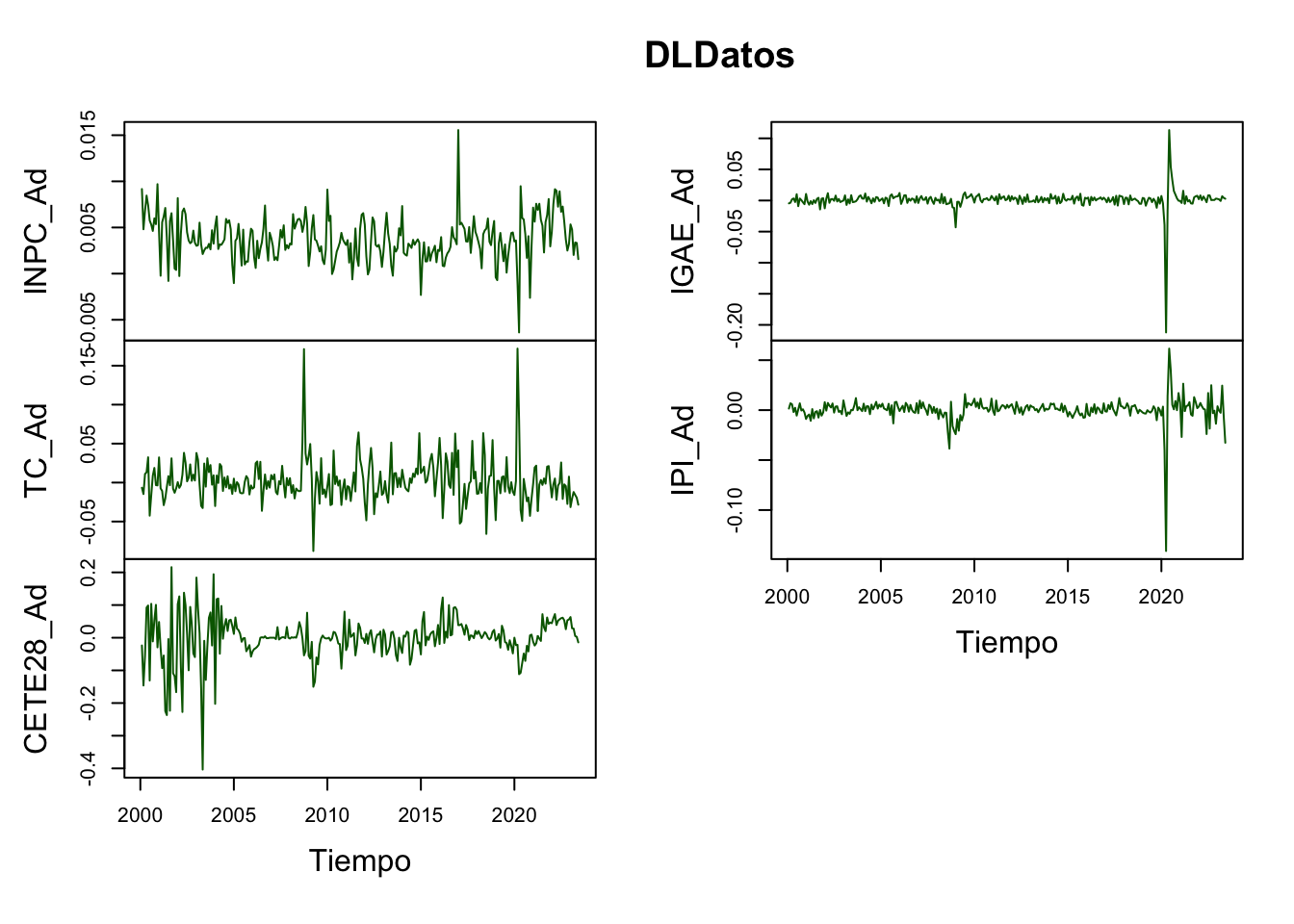

. Para ejemplificar el procedimiento de cointegración utilizaremos las series de INPC, Tipo de Cambio, rendimiento de los Cetes a 28 días, IGAE e Índice de Producción Industrial de Estados Unidos. Quizá el marco teórico de la relación entre las variables no sea del todo correcto, pero dejando de lado ese problema, estimaremos si las 5 series cointegran.

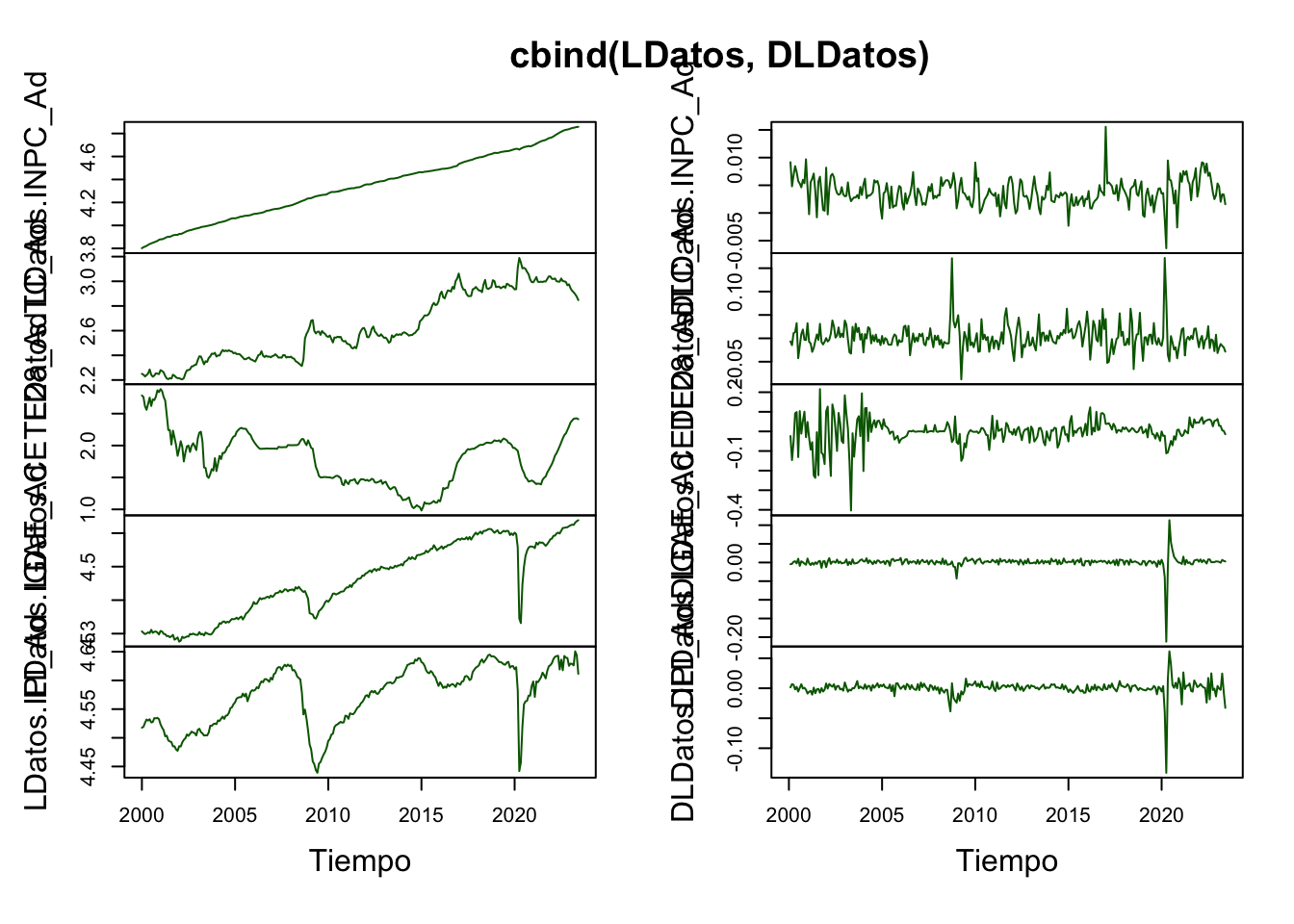

Por principio, probaremos que todas las series son I(1), lo cual es cierto (ver Scrip para mayores detalles). En las Figuras 5.9, 5.10 y 5.11 se muestran las series en niveles y en diferencias, con lo cual ilustramos como es viable que las series sean I(1).

library(ggplot2)

library(dplyr)

library(stats)

library(MASS)

library(strucchange)

library(zoo)

library(sandwich)

library(urca)

library(lmtest)

library(vars)

#

load("BD/Datos_Ad.RData")

#

## Conversion a series de tiempo:

Datos <- ts(Datos_Ad[7: 11],

start = c(2000, 1),

freq = 12)

LDatos <- log(Datos)

DLDatos <- diff(log(Datos, base = exp(1)),

lag = 1,

differences = 1)plot(LDatos,

plot.type = "m", nc = 2,

col = c("darkgreen", "darkblue", "darkred", "orange", "purple"),

#main = "Series en Logaritmos",

xlab = "Tiempo")

Figure 5.9: Series en niveles (logaritmos) para la prueba de Cointegración

plot(DLDatos,

plot.type = "m", nc = 2,

col = c("darkgreen", "darkblue", "darkred", "orange", "purple"),

#main = "Series en Diferencias Logaritmicas",

xlab = "Tiempo")

Figure 5.10: Series en Diferencias Logarítmicas para la prueba de Cointegración

plot(cbind(LDatos, DLDatos),

plot.type = "m", nc = 2,

col = c("darkgreen", "darkblue", "darkred", "orange", "purple"),

#main = "Comparacion de Series en Diferencias",

xlab = "Tiempo")

Figure 5.11: Comparacion de Series en Diferencias para la prueba de Cointegración

Posteriormente, determinamos cuál es el orden adecuado de un VAR(p) en niveles. En el Cuadro 5.8 mostramos los resultados de los criterios de información para determinar el número de rezagos óptimos, el cual resultó en \(p = 3\) para los criterios AIC y FPE, \(p = 2\) para el criterio HQ y \(p = 1\) para el criterio SC. Por lo tanto, decidiremos utilizar un VAR(3) con tendencia y constante. Note que es posible elegir otros modelos de VAR que incluyan: solo tendencia, solo constante o ninguno de estos elementos.

| Rezagos | AIC | HQ | SC | FPE |

|---|---|---|---|---|

| 1 | -4.606707e+01 | -4.585260e+01 | -4.553568e+01 | 9.848467e-21 |

| 2 | -4.643287e+01 | -4.606521e+01 | -4.552191e+01 | 6.834064e-21 |

| 3 | -4.647783e+01 | -4.595697e+01 | -4.518730e+01 | 6.539757e-21 |

| 4 | -4.645834e+01 | -4.578428e+01 | -4.478824e+01 | 6.679778e-21 |

## $selection

## AIC(n) HQ(n) SC(n) FPE(n)

## 3 2 2 3

##

## $criteria

## 1 2 3 4 5

## AIC(n) -4.313083e+01 -4.356687e+01 -4.357973e+01 -4.350356e+01 -4.346656e+01

## HQ(n) -4.294456e+01 -4.324754e+01 -4.312735e+01 -4.291813e+01 -4.274808e+01

## SC(n) -4.266685e+01 -4.277147e+01 -4.245291e+01 -4.204533e+01 -4.167692e+01

## FPE(n) 1.855848e-19 1.200259e-19 1.185548e-19 1.280605e-19 1.330869e-19

## 6 7 8 9 10

## AIC(n) -4.336621e+01 -4.335767e+01 -4.344758e+01 -4.337426e+01 -4.336604e+01

## HQ(n) -4.251468e+01 -4.237309e+01 -4.232994e+01 -4.212358e+01 -4.198230e+01

## SC(n) -4.124515e+01 -4.090520e+01 -4.066369e+01 -4.025896e+01 -3.991931e+01

## FPE(n) 1.474594e-19 1.491718e-19 1.368875e-19 1.480478e-19 1.502148e-19## $selection

## AIC(n) HQ(n) SC(n) FPE(n)

## 3 2 2 3

##

## $criteria

## 1 2 3 4 5

## AIC(n) -4.302183e+01 -4.347336e+01 -4.349266e+01 -4.344039e+01 -4.340559e+01

## HQ(n) -4.286217e+01 -4.318065e+01 -4.306689e+01 -4.288157e+01 -4.271372e+01

## SC(n) -4.262413e+01 -4.274425e+01 -4.243213e+01 -4.204844e+01 -4.168223e+01

## FPE(n) 2.069525e-19 1.317817e-19 1.293226e-19 1.363788e-19 1.414042e-19

## 6 7 8 9 10

## AIC(n) -4.332101e+01 -4.330189e+01 -4.336318e+01 -4.331231e+01 -4.328931e+01

## HQ(n) -4.249609e+01 -4.234392e+01 -4.227216e+01 -4.208823e+01 -4.193218e+01

## SC(n) -4.126624e+01 -4.091570e+01 -4.064558e+01 -4.026328e+01 -3.990887e+01

## FPE(n) 1.541996e-19 1.576227e-19 1.488111e-19 1.573361e-19 1.619720e-19## $selection

## AIC(n) HQ(n) SC(n) FPE(n)

## 3 2 2 3

##

## $criteria

## 1 2 3 4 5

## AIC(n) -4.305293e+01 -4.349519e+01 -4.350862e+01 -4.345110e+01 -4.341448e+01

## HQ(n) -4.289327e+01 -4.320248e+01 -4.308286e+01 -4.289228e+01 -4.272261e+01

## SC(n) -4.265523e+01 -4.276608e+01 -4.244809e+01 -4.205915e+01 -4.169111e+01

## FPE(n) 2.006156e-19 1.289360e-19 1.272744e-19 1.349265e-19 1.401536e-19

## 6 7 8 9 10

## AIC(n) -4.332555e+01 -4.330697e+01 -4.337250e+01 -4.331647e+01 -4.329111e+01

## HQ(n) -4.250063e+01 -4.234899e+01 -4.228147e+01 -4.209239e+01 -4.193398e+01

## SC(n) -4.127078e+01 -4.092077e+01 -4.065489e+01 -4.026744e+01 -3.991067e+01

## FPE(n) 1.535010e-19 1.568252e-19 1.474313e-19 1.566830e-19 1.616817e-19## $selection

## AIC(n) HQ(n) SC(n) FPE(n)

## 3 2 2 3

##

## $criteria

## 1 2 3 4 5

## AIC(n) -4.300965e+01 -4.346535e+01 -4.349616e+01 -4.344160e+01 -4.339782e+01

## HQ(n) -4.287660e+01 -4.319924e+01 -4.309701e+01 -4.290939e+01 -4.273256e+01

## SC(n) -4.267824e+01 -4.280252e+01 -4.250191e+01 -4.211594e+01 -4.174075e+01

## FPE(n) 2.094860e-19 1.328347e-19 1.288547e-19 1.361851e-19 1.424605e-19

## 6 7 8 9 10

## AIC(n) -4.331937e+01 -4.328561e+01 -4.334269e+01 -4.329813e+01 -4.326892e+01

## HQ(n) -4.252106e+01 -4.235424e+01 -4.227828e+01 -4.210066e+01 -4.193840e+01

## SC(n) -4.133088e+01 -4.096570e+01 -4.069137e+01 -4.031539e+01 -3.995476e+01

## FPE(n) 1.543800e-19 1.601088e-19 1.517650e-19 1.594144e-19 1.650919e-19El mismo número de rezagos los utilizaremos para probar la Cointegración, ya sea por una estadística de la Traza o por una del máximo valor propio. Dado que los resultados se sostienen, sólo mostraremos uno de los casos en que las series cointegran y únicamente para el caso de la prueba de la traza (el otro caso está disponible en el código de R disponible abajo). En el Cuadro 5.9 reportamos los resultados del Test de Cointegración para un modelo con 3 rezagos.

Cuadro: (#tab:TrazaTest) Prueba de la traza para cointegración considerando un VAR(p) con término constante y tendencia de las series \(LINPC_t\), \(LTC_t\), \(LCETE28_t\), \(LIGAE_t\) y \(LIPI_t\).

| r \(\leq\) | Estadística | 10% | 5% | 1% |

|---|---|---|---|---|

| 4 | 4.79 | 10.49 | 12.25 | 16.26 |

| 3 | 13.97 | 22.76 | 25.32 | 30.45 |

| 2 | 27.45 | 39.06 | 42.44 | 48.45 |

| 1 | 48.14 | 59.14 | 62.99 | 70.05 |

| 0 | 118.98 | 83.20 | 87.31 | 96.58 |

Los resultados del Cuadro 5.9 indican que aceptamos la hipótesis nula para el caso de \(r \leq 1\) al \(5\%\), por lo que podemos concluir que existe evidencia estadística para probar que existe al menos 1 vector de cointegración. Por lo que dicho vector normalizado a la primera entrada es: \[\begin{equation} \boldsymbol{\beta} = \left[ \begin{matrix} 1.00000000 \\ 0.2100057 \\ 0.4812626 \\ -2.8386112 \\ -1.2576912 \\ 14.2887887 \\ \end{matrix} \right] \end{equation}\]

Donde el vector esta normalizado para la serie \(LINPC_t\), por lo que concluímos que la relación de largo plazo que encontramos cointegra estará dada por: \[\begin{eqnarray*} LINPC_t & = & -0.2100057 LTC_t - 0.4812626 LCETE28_t \\ & & + 2.8386112 LIGAE_t + 1.2576912 LIPI_t \\ & & - 14.2887887 \end{eqnarray*}\]

## VAR Estimacion:

VAR_1 <- VAR(LDatos, p = 3, type = "both")

#summary(VAR_1)

#plot(VAR_1, names = "INPC_Ad")

#plot(VAR_1, names = "TC_Ad")

#plot(VAR_1, names = "CETE28_Ad")

#plot(VAR_1, names = "IGAE_Ad")

#plot(VAR_1, names = "IPI_Ad")

# Cointegration Test:

#ca.jo = function (x, type = c("eigen", "trace"), ecdet = c("none", "const",

#"trend"), K = 2, spec = c("longrun", "transitory"), season = NULL,

#dumvar = NULL)

#summary(ca.jo(LDatos, type = "trace", ecdet = "trend", K = 3, spec = "longrun"))

#summary(ca.jo(LDatos, type = "trace", ecdet = "const", K = 3, spec = "longrun"))

#summary(ca.jo(LDatos, type = "trace", ecdet = "none", K = 3, spec = "longrun"))

CA_1 <- ca.jo(LDatos, type = "trace", ecdet = "const", K = 3, spec = "longrun")

summary(CA_1)##

## ######################

## # Johansen-Procedure #

## ######################

##

## Test type: trace statistic , without linear trend and constant in cointegration

##

## Eigenvalues (lambda):

## [1] 2.242278e-01 7.148297e-02 4.716974e-02 3.235583e-02 1.703739e-02

## [6] 3.730682e-17

##

## Values of teststatistic and critical values of test:

##

## test 10pct 5pct 1pct

## r <= 4 | 4.79 7.52 9.24 12.97

## r <= 3 | 13.97 17.85 19.96 24.60

## r <= 2 | 27.45 32.00 34.91 41.07

## r <= 1 | 48.14 49.65 53.12 60.16

## r = 0 | 118.98 71.86 76.07 84.45

##

## Eigenvectors, normalised to first column:

## (These are the cointegration relations)

##

## INPC_Ad.l3 TC_Ad.l3 CETE28_Ad.l3 IGAE_Ad.l3 IPI_Ad.l3

## INPC_Ad.l3 1.0000000 1.0000000 1.0000000 1.000000 1.00000000

## TC_Ad.l3 0.2100057 0.3958412 0.6038714 -3.946863 -0.66160415

## CETE28_Ad.l3 0.4812626 -0.3505729 0.2932620 1.025381 0.02134859

## IGAE_Ad.l3 -2.8386112 -4.9448228 -4.1431506 10.685831 -1.62038123

## IPI_Ad.l3 -1.2576912 0.8682351 2.2789480 -19.080015 1.60589077

## constant 14.2887887 13.2882018 1.6072247 43.673551 -2.75645487

## constant

## INPC_Ad.l3 1.00000000

## TC_Ad.l3 -0.84381863

## CETE28_Ad.l3 0.06866727

## IGAE_Ad.l3 1.32792512

## IPI_Ad.l3 -3.05544132

## constant 5.81151022

##

## Weights W:

## (This is the loading matrix)

##

## INPC_Ad.l3 TC_Ad.l3 CETE28_Ad.l3 IGAE_Ad.l3

## INPC_Ad.d 0.001551917 4.896886e-05 0.0002254138 -0.0001685412

## TC_Ad.d 0.002200808 -5.756379e-03 -0.0293306746 -0.0003866727

## CETE28_Ad.d -0.009399815 -2.250446e-02 -0.0166361225 -0.0160384399

## IGAE_Ad.d 0.001105776 1.441007e-02 0.0023574644 -0.0015712694

## IPI_Ad.d 0.001442047 1.286402e-02 -0.0014986278 -0.0011379265